What Bank Earnings Reveal About The Economy, The Consumer, and Credit Appetite

The Rithm Take

Bottom Line: Q2 showed a banking system getting more precise about where it extends credit. Corporates are levering up at current funding costs, and banks are meeting that demand. NBFI lending is turning into a relationship business like commercial loans with deposits and payments attached, making it stickier than a simple credit exposure. Lenders are underwriting the AI buildout piece by piece. On the consumer, the signal this quarter is whether a bank's provision beat came from fewer losses or from releasing reserves. Across all four threads, credit is expanding on the lender's terms, not the borrower's.

Every large bank beat on revenue and provisions this quarter. That headline reads like a system-wide credit reopening. But the banking system extended more credit to the parts of the economy asking for it with confidence, and pulled back its risk appetite in the parts where it didn't like what it saw.

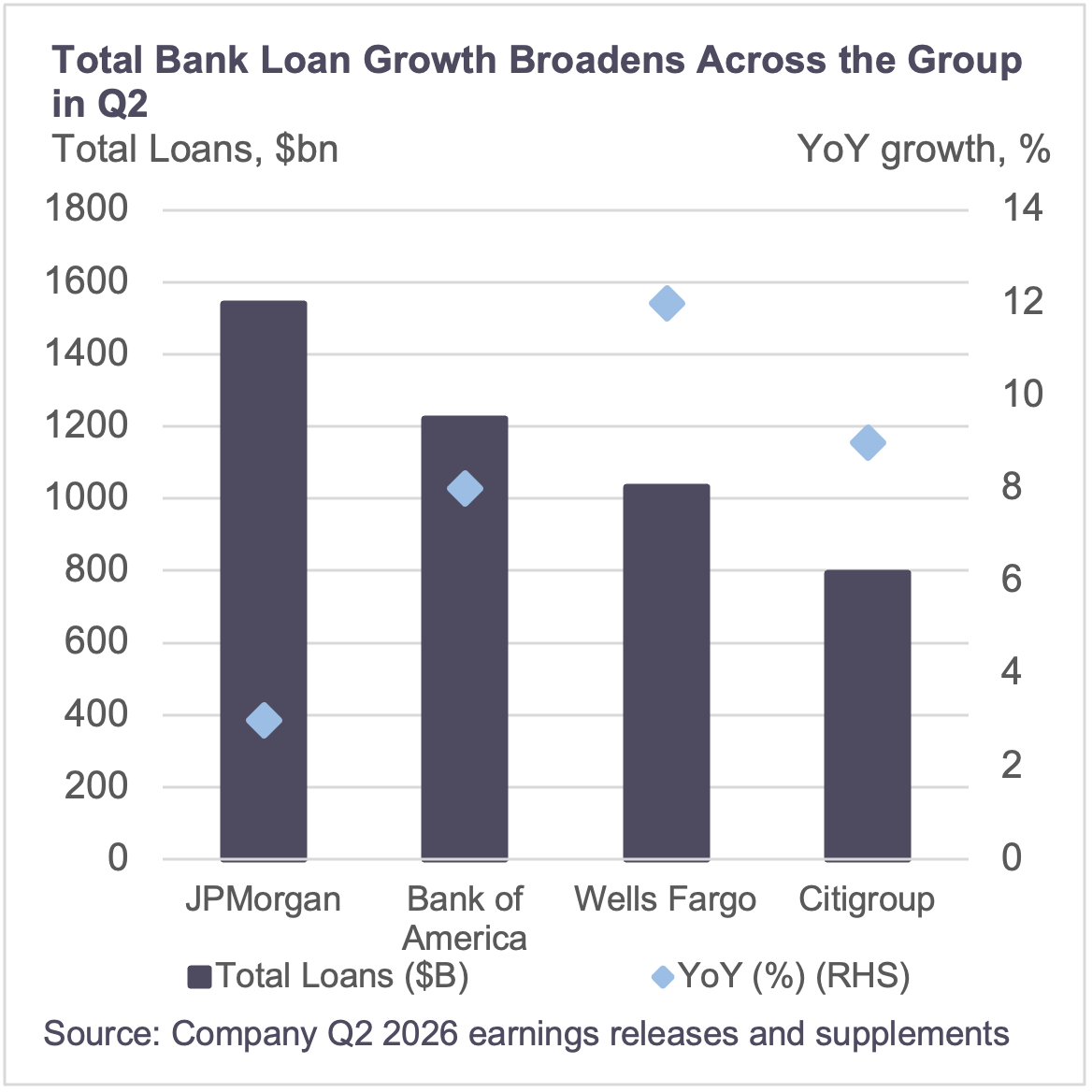

The clearest evidence is in commercial and industrial lending. Bank of America's book grew broadly across regions and industries rather than around a handful of large deals. Corporate borrowers are levering up at current funding costs, a sign of confidence heading into the second half. Wells Fargo's growth was faster, but a real share of it reflects the balance sheet catching up after its asset cap came off, mechanical catch-up more than organic demand.

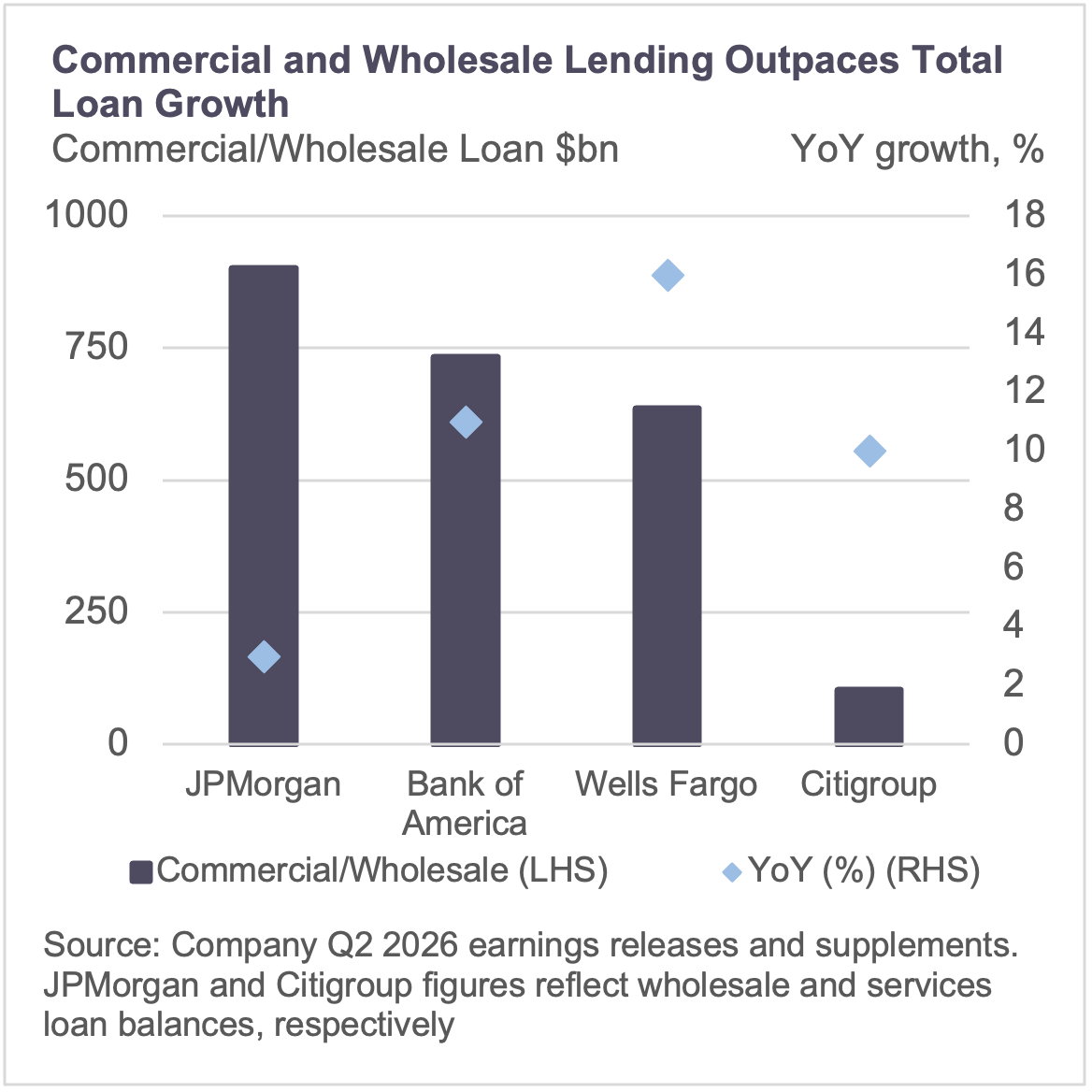

NBFI lending is where the more durable shift is happening. This quarter JPMorgan described it as a source of deposit creation, a similar relationship dynamic that has long applied to C&I lending, where a lending relationship anchors the borrower's deposit and payments business. Wells Fargo's disclosure of its business credit intermediary book showed the exposure has grown large enough to function as a franchise on its own. NBFI lending is starting to carry relationship weight, with deposits and payments revenue riding alongside the credit rather than the credit standing alone.

The most underappreciated signal this quarter is in how banks are underwriting the AI buildout. The underwriting itself tells a more granular story than the aggregate capex numbers do. Wells Fargo is pricing power, chips, and construction risk as separate credits with separate repayment timelines, and JPMorgan walked away from specific data center deals over power availability, ahead of any default showing up anywhere in the market. Credit underwriting is differentiating the AI infrastructure that gets paid back on schedule from the parts that carry more risk.

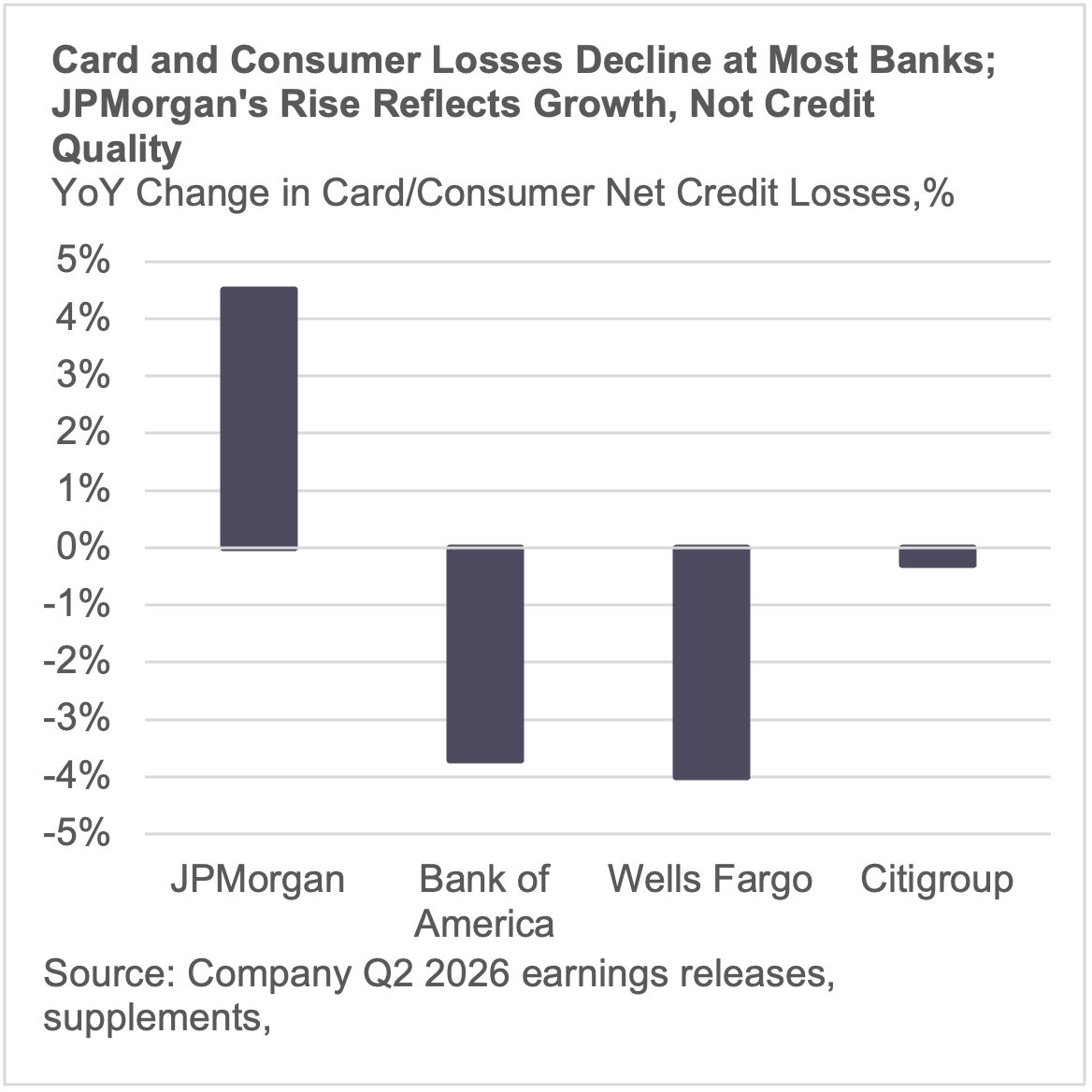

On the consumer, this quarter added a wrinkle to the K-shaped narrative rather than confirming or disproving it outright. JPMorgan and Wells Fargo both said they aren't seeing meaningful delinquency divergence by FICO score or income cohort. Citi's cards miss and elevated loss guide are the one result in the group that doesn't fit that pattern, though the more precise read isn't that Citi's credit is deteriorating, it's that the bank's provision decisions aren't fully supported by what its own numbers show, explained below.

Provision quality still varied by bank. Wells Fargo's beat came almost entirely from lower realized losses, a genuine improvement in credit performance. Citi's provision beat leaned on a $232 million reserve release inside its card book, even as net credit losses in that segment stayed essentially flat year over year and its reserve coverage ratio fell 40 basis points. One bank saw fewer of its borrowers actually default. The other set aside less money against defaults it expects later, without losses actually improving to justify it.

Market Signals

Corporate borrowing reflects confidence, not just cheaper funding. C&I demand grew broadly rather than around a handful of large deals, evidence that corporates are levering up at current rates on their own initiative. Bank of America's 11% growth is the cleanest read of that demand; Wells Fargo's faster growth is partly mechanical, reflecting balance sheet catch-up after its asset cap lifted.

Card and consumer credit losses fell at three of four banks, and the one exception explains itself. Bank of America and Wells Fargo both show real declines in card and consumer net credit losses, down 3.7% and 4.0% year over year. JPMorgan's card losses rose 4.5% in dollar terms, but that's a function of a growing card book, since JPMorgan's own loss rate actually improved over the same period.