AI Repricing: Equities, Credit, and the Cost of Capital

The Rithm Take

The Bottom Line: AI capex is now large enough to move GDP on its own. That growth is increasingly funded by capital markets, not cash flow. Hyperscalers are issuing record debt and equity, at scale and cost that were not part of the trade a year ago, and lengthening the duration of that debt to match the life of the assets it funds. Equity investors are rewarding the physical AI buildout over the hyperscalers themselves, and credit markets are pricing software risk higher for the first time in a decade. Capital is not leaving the AI trade. It is discriminating within it. Selection is the setup for the back half of the year.

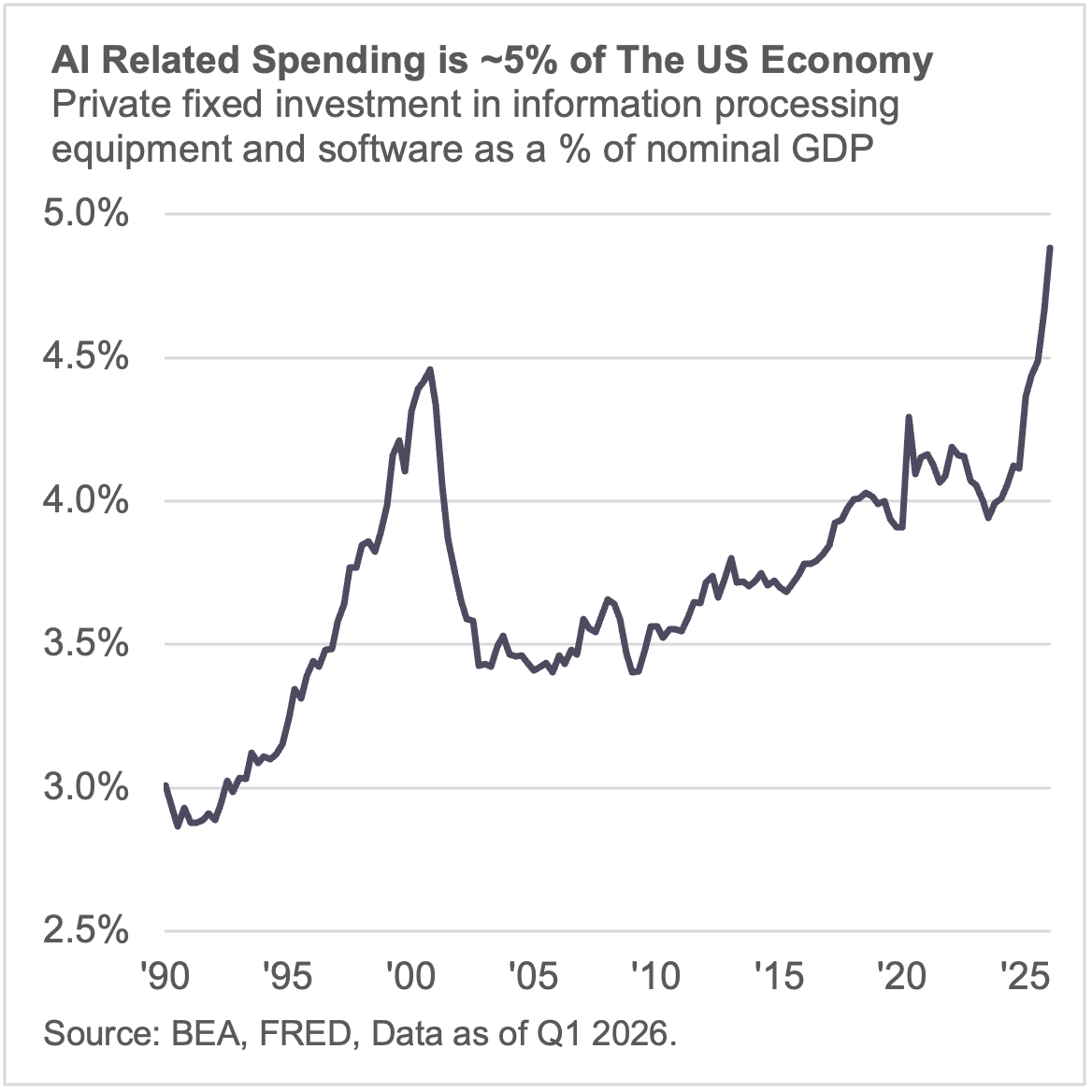

The AI buildout is now carrying the economy to a degree with no modern precedent, including the late 1990s, by certain metrics. In Q1, AI-related capex is around 5% of GDP, computer/peripheral equipment plus software alone added roughly 1.1 of the 2.0 percentage points of growth; strip the AI surge out and Q1 lands near 1%.

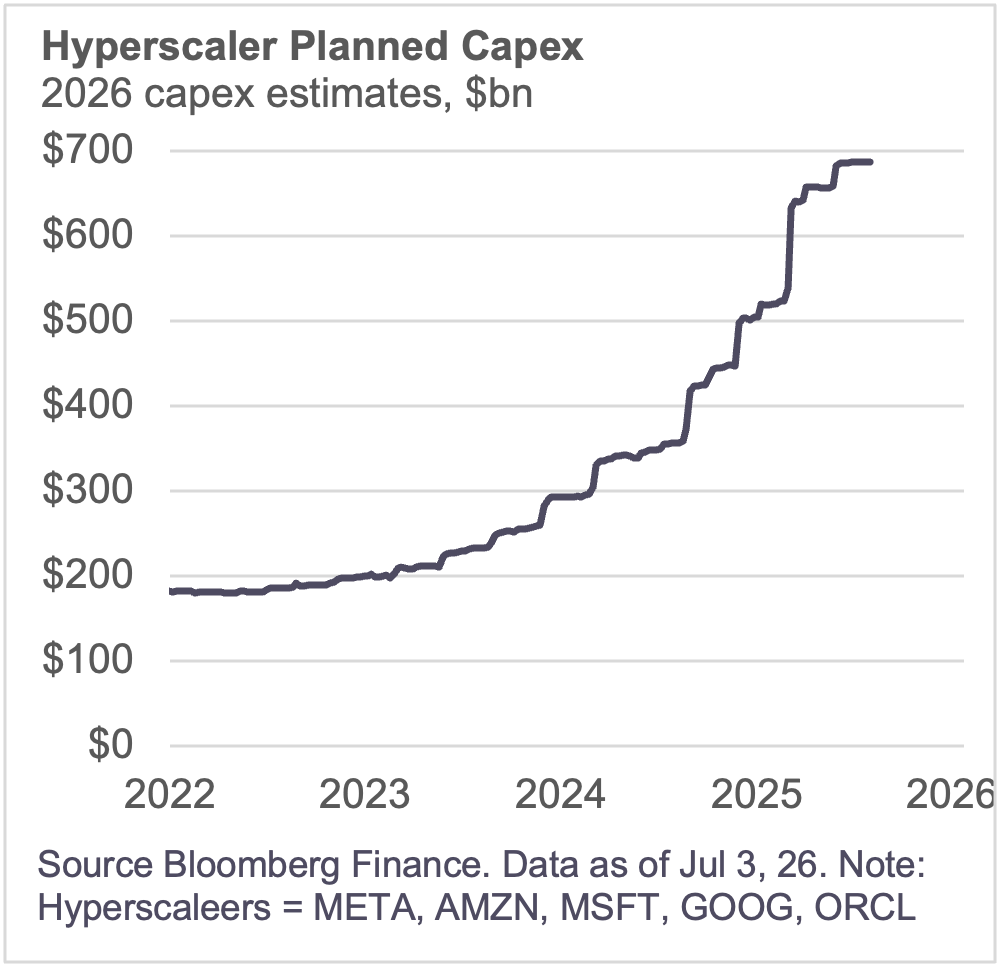

The hyperscalers (companies providing cloud infrastructure for AI processes) have guided to ~$700bn of capex this year, nearly doubling year-over-year.

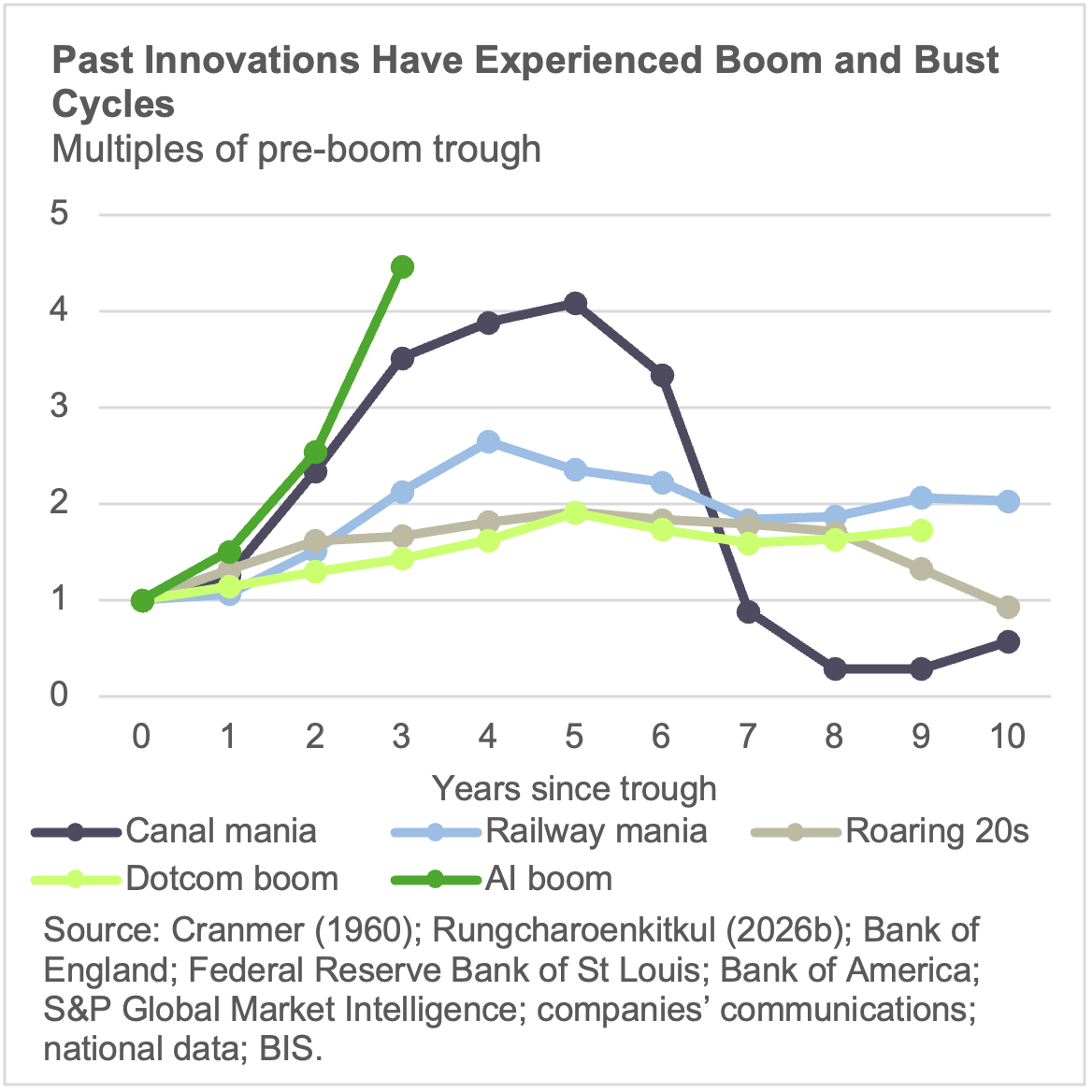

While the consensus in the market is that AI will be a transformational general-purpose technology (GPT), participants have become weary of the costs associated with its buildout. Especially considering the boom and bust buildouts of other successful transformational GPT’s.

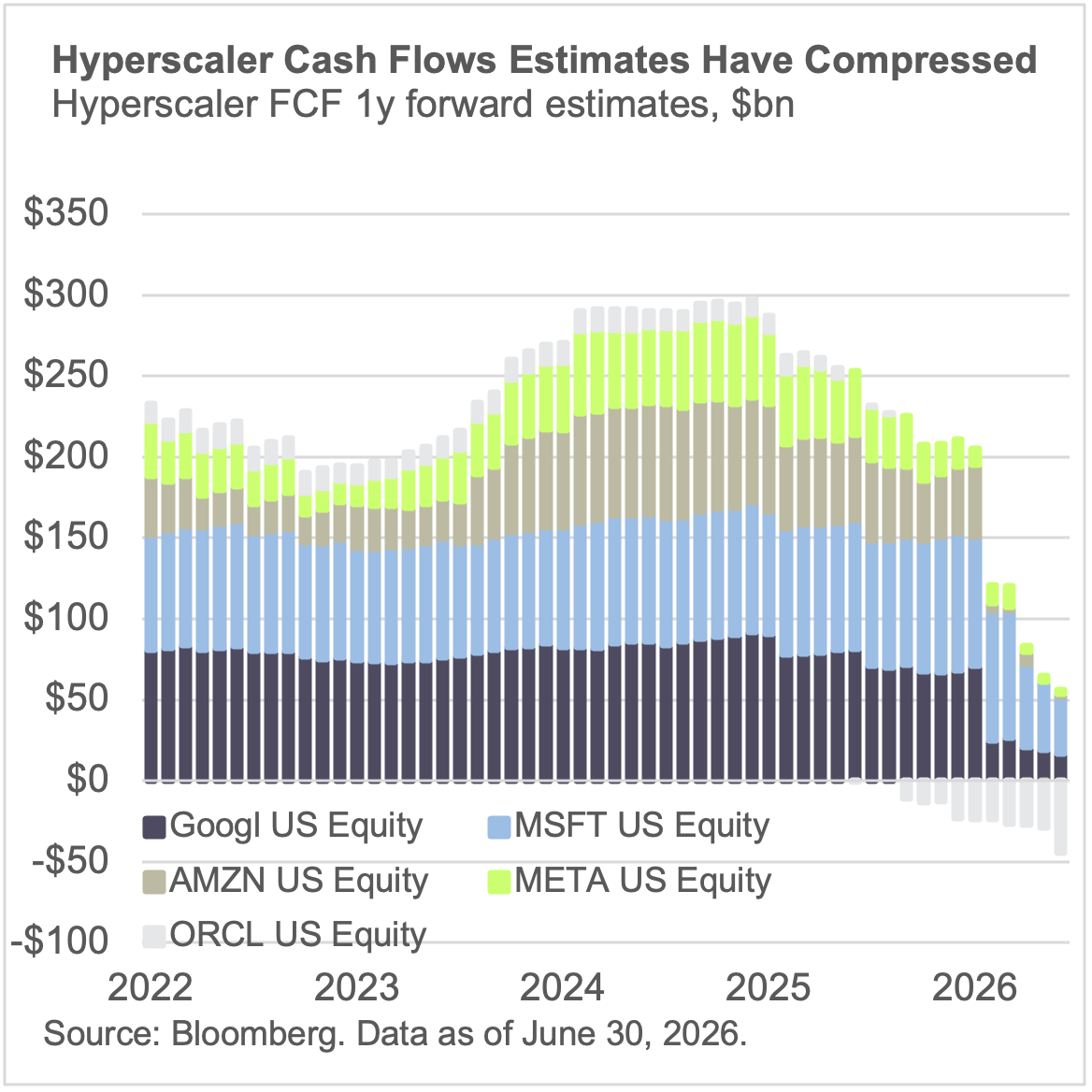

What’s more are the hyperscalers, whose fee-based capital light business model, is now shifting towards capital heavy as the buildout of data centers accelerates. That has compressed the massive free cash flows of these companies markedly and in some cases turning them negative.

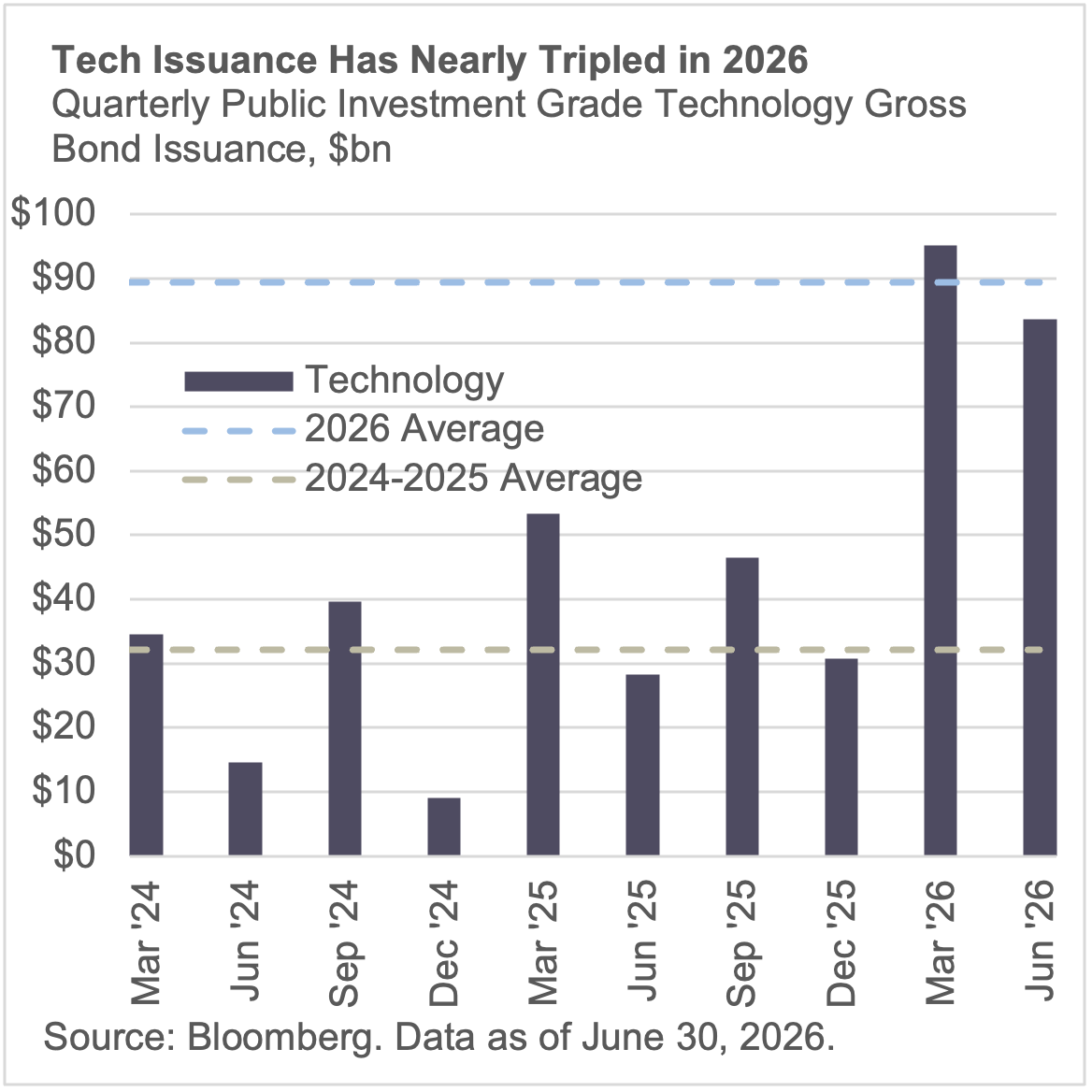

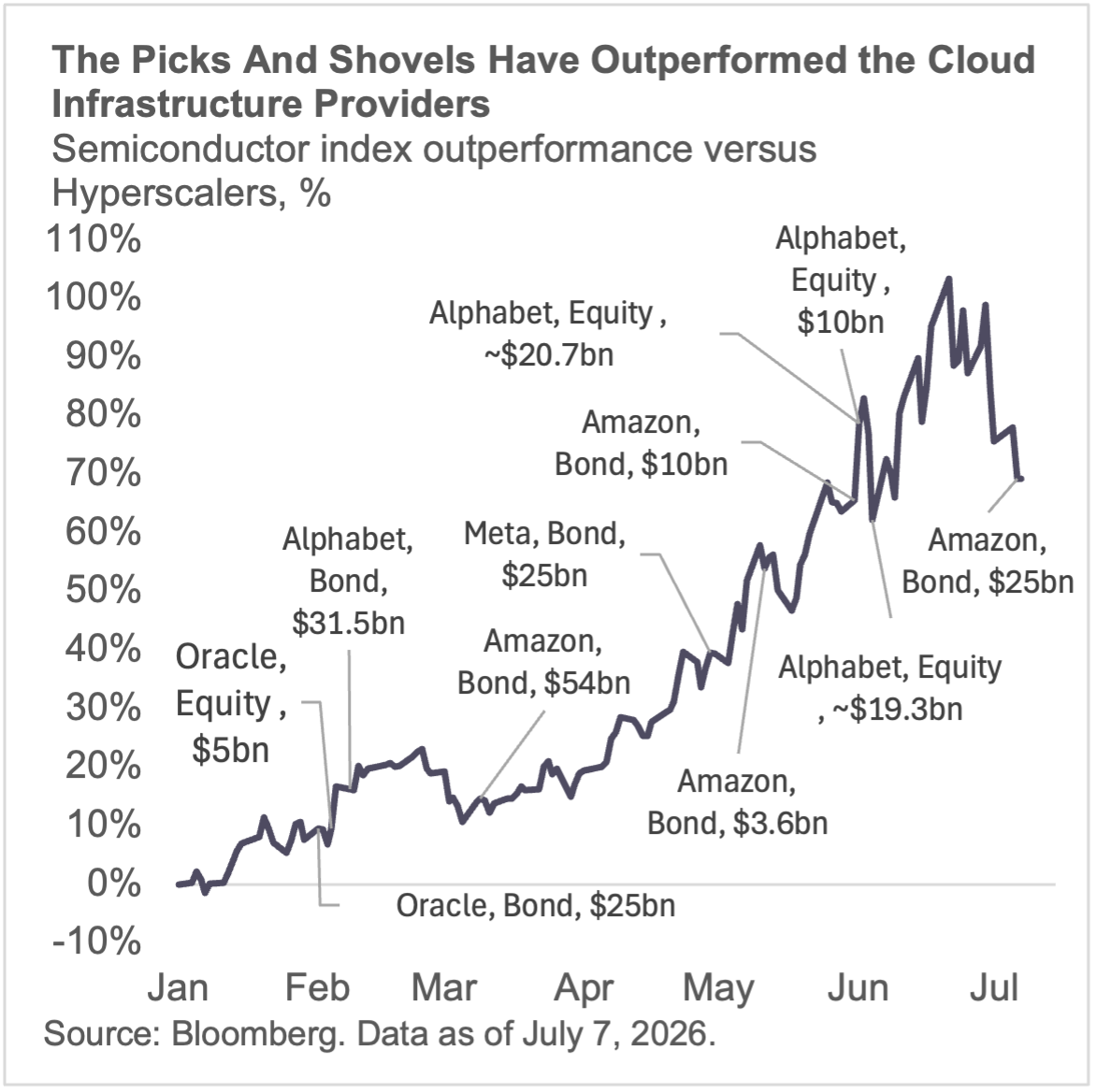

This compression of cash flow has caused the hyperscalers to seek external capital to continue the funding of the AI infrastructure buildout. Amazon's March deal ($54bn combined) broke the record for the largest corporate bond sale ever, surpassing Verizon's $49bn 2013 offering — which stood as the record for over a decade. Alphabet's February sale included the first 100-year bond issued by a technology company since Motorola in 1997. And per Reuters, high-quality AI debt issuance by hyperscalers has already surpassed the 2025 annual volume.

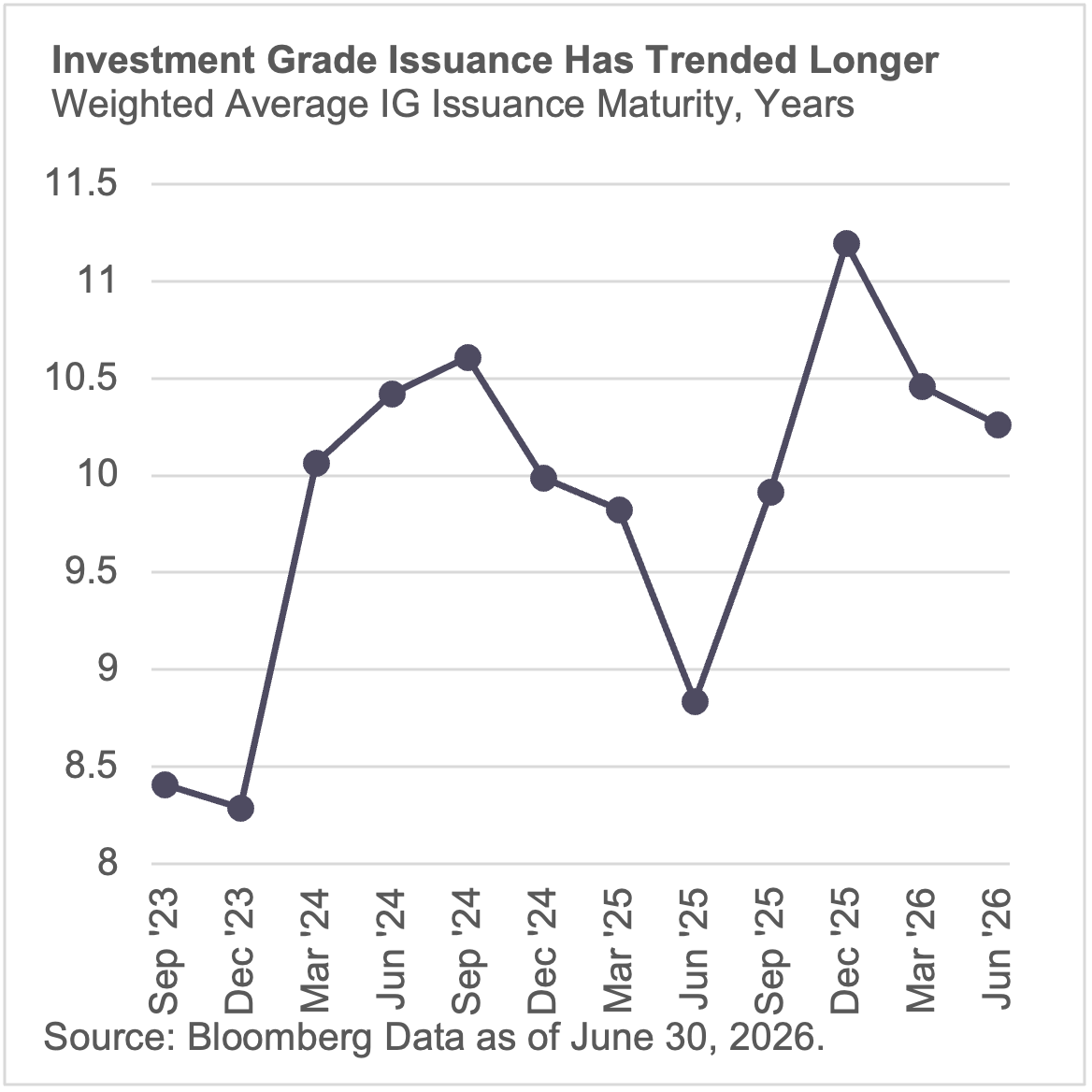

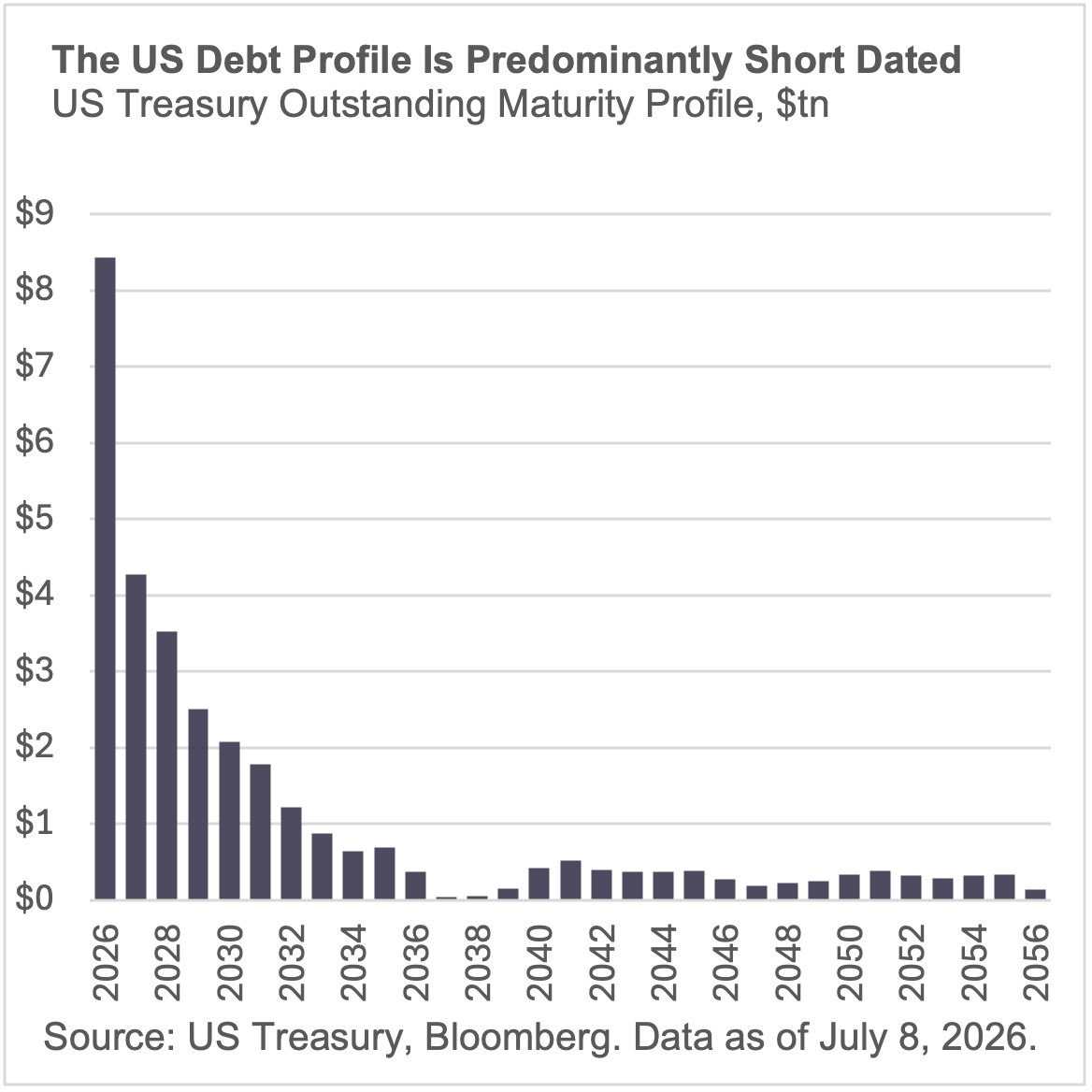

Investment grade issuance has also grown longer dated, matching the multi-decade liability profiles of AI infrastructure projects like data centers. The weighted average maturity of investment grade issuance has extended to over 10 years in June, up from just over eight years in 2023. Treasuries are moving the opposite direction, shortening average maturity to minimize borrowing costs against an upward sloping yield curve. The result is a growing divergence across the two pools of high-quality debt: corporate credit lengthening while sovereign debt shortens. Hyperscaler issuance plans into Q2 earnings season are the next test of how investors resolve that divergence.

Equity markets have taken notice, and have shifted allocations towards the beneficiaries of AI spending including chipmakers, away from the hyperscalers. The SOX semiconductor index is now outperforming the hyperscalers by ~70% year-to-date.

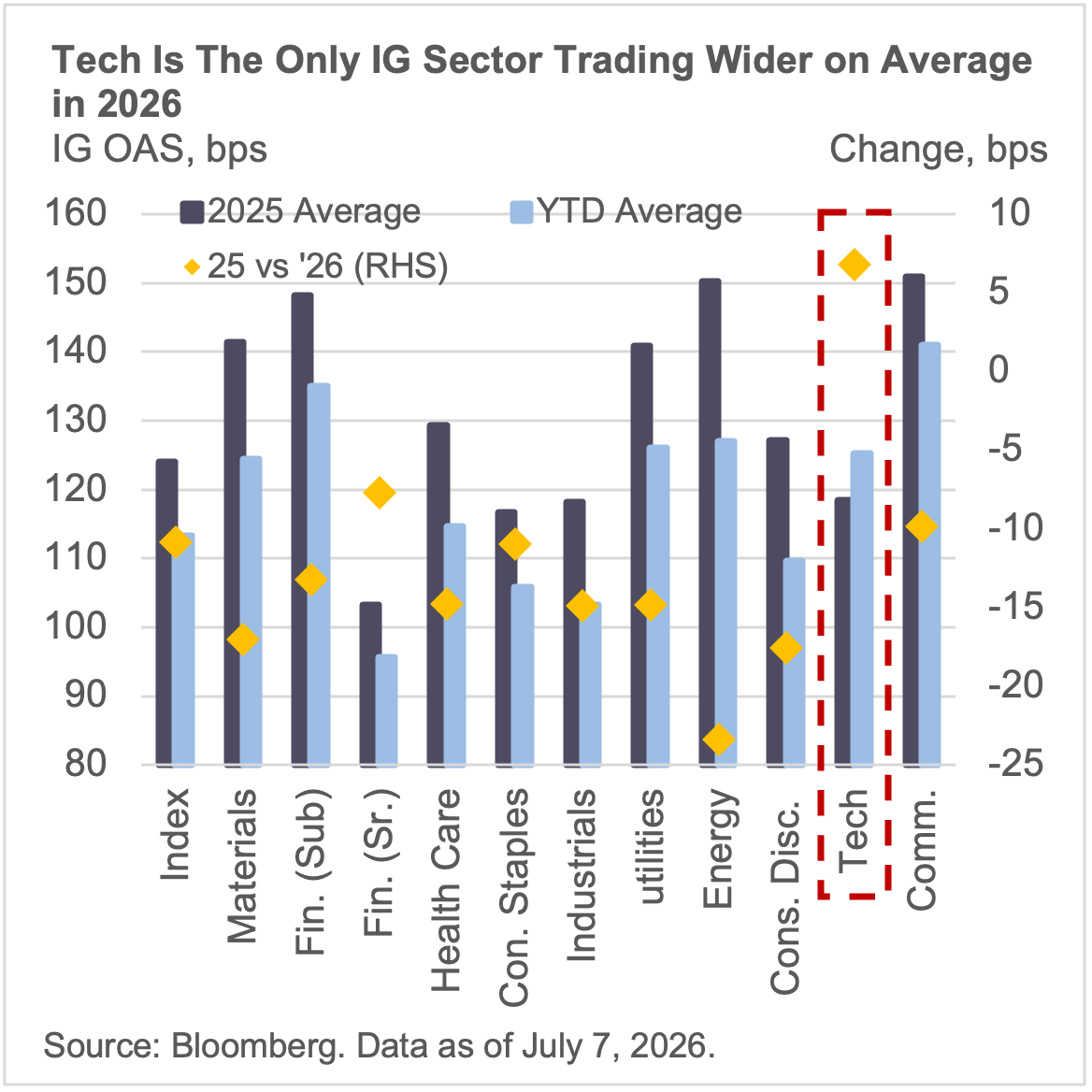

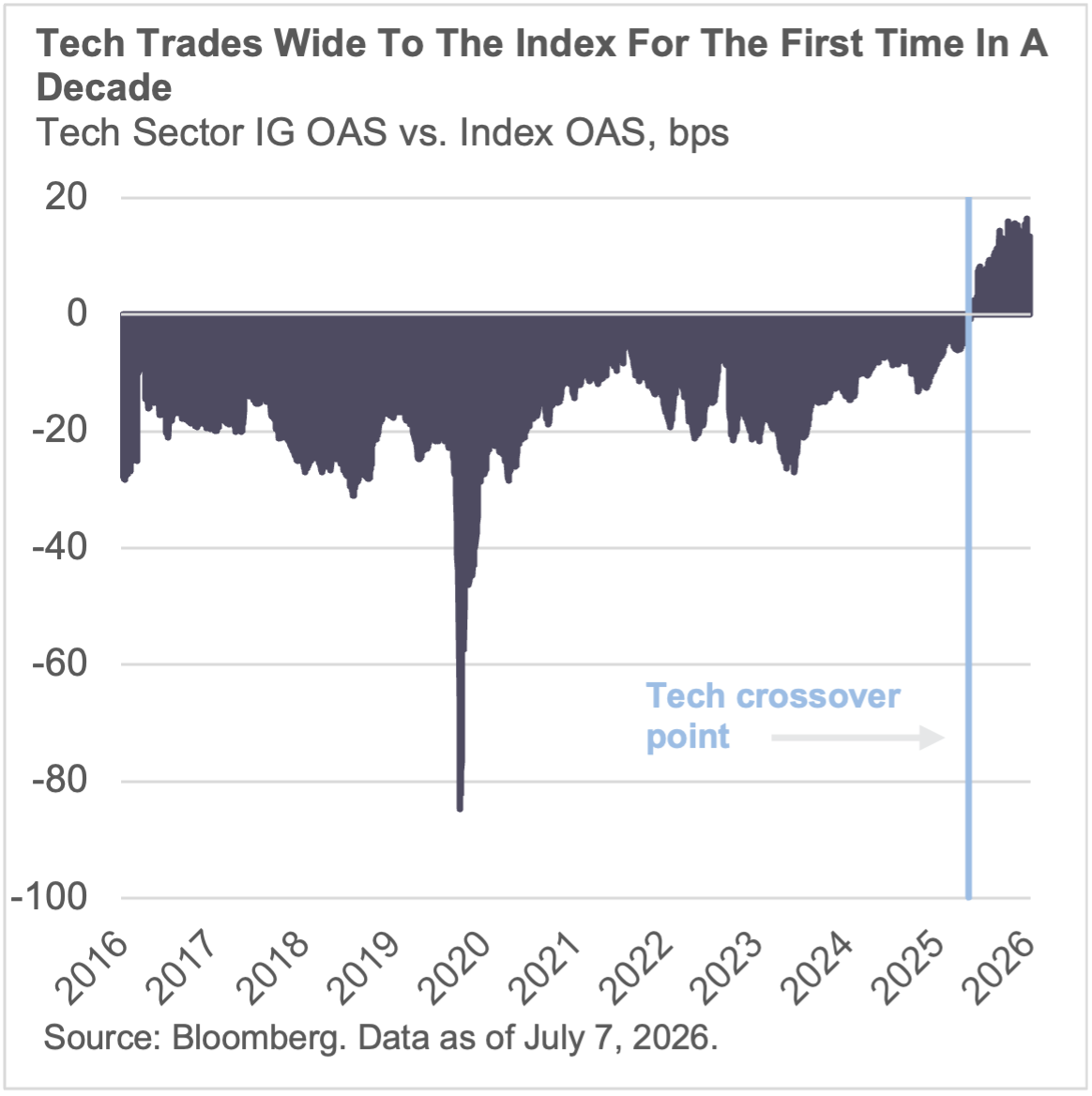

In credit markets, tech underperformance is even clearer. Year-to-date, technology is the only investment-grade sector trading wider than its 2025 average spread — a sector that traded tight to the index on 100% of trading days over the past decade until late last year.

Capital is discriminating within the AI trade. Hyperscalers can still raise capital at scale, but at more expensive levels and longer duration. The physical AI buildout is still being rewarded. Software is being priced for risk it did not carry a year ago.

This is a market rewarding selection. Active selection is the theme for the back half of the year. Alpha will come from underwriting the trade, not from owning it broadly.