Warsh at the Helm: Three Signals to Watch

The Rithm Take

The FOMC will meet for the first time with Kevin Warsh as Chair this Wednesday. While markets assign virtually no probability to a rate move, the meeting will be closely watched for signals on the Fed’s communication strategy, Warsh’s tone relative to his confirmation hearing, and the future path of the balance sheet.

The meeting

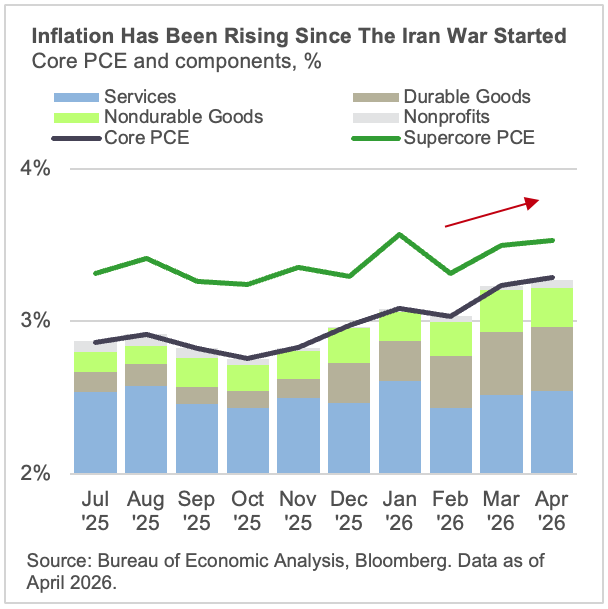

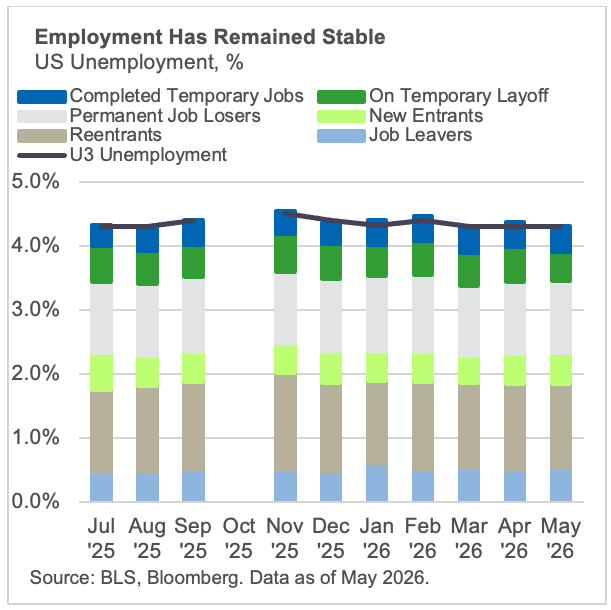

The committee is meeting with their preferred inflation measure, Core PCE, well above it’s 2% target at 3.28%. The employment side of the mandate appears comparatively stable: the unemployment rate has remained within a 50 bp range since May 2024 and has held at 4.3% for three months, a level likely close to full employment.

Kevin Warsh at the helm: what we’re watching

- Fed Communication: One of the Fed’s key policy tools is forward guidance – telling the public about the likely future course of monetary policy. Chair Warsh has the opinion that the Fed’s usage of the tool has been excessive. In his view, dot plots, frequent speeches, and predictable press conferences can lock policymakers into stale forecasts and reduce flexibility. Chair Warsh has a similar opinion on the dot plot and Summary of Economic Projections (SEP), in that policy makers may be more tied to forecasts based on their prior responses. While both the dots and SEP would need committee approval to remove them from the quarterly output, Chair Warsh would have the ability to deemphasize their importance.

All else equal, less intra-meeting communication would likely increase market volatility during FOMC meeting days and decisions. - Balance sheet: Chair Warsh has been a critic of the Fed’s balance sheet expansion. He has said that QE1 after the financial crisis was an appropriate response to a crisis, but has been critical on the failure to reduce the balance sheet outside of crisis times. During his confirmation hearing Warsh proposed shrinking the balance sheet slowly and deliberately. Warsh’s preference seems to be for a smaller balance sheet, less MBS exposure over time, and shorter duration Treasuries to closer duration match liabilities.

There exists a limit to how far the Fed can shrink the balance sheet. The major liabilities on the Fed balance sheet are made up of currency in circulation, the Treasury General Account (TGA), reverse repo and reserve balances held by depository institutions. Currency in circulation is a function of demand in the economy and can’t be directly controlled by the Fed, and the Fed does not control the TGA. What’s more, there is a practical limitation as to how far the Fed can reduce reserves while operating in an ample reserve framework – that limit is not known until after the fact when stress appears in funding markets. As with communications policy, Warsh will have limited unilateral authority. Balance sheet policy is ultimately an FOMC decision, not something dictated solely by the Chair. - The tone: The final focal point will be Warsh’s tone, particularly given his historical reputation as an inflation-sensitive policymaker, and how it compares with his Senate confirmation hearing. Warsh’s confirmation hearing was not hawkish in the sense of signaling imminent hikes. It was better understood as an effort to establish anti-inflation credibility and Fed independence while avoiding a near-term rate commitment. The surprise was the absence of a dovish rate-cut argument, especially given political pressure for lower rates. For the first press conference, the relevant comparison is whether he stays in that inflation-first but noncommittal lane, or moves meaningfully toward either a hike-tolerant hawkish posture.

The inflation data which has come since his confirmation hearing will give Warsh cover, should he so choose to lean on the hawkish side. A hawkish presser could re-anchor Fed independence, but just last week President Trump said “There's no reason to raise interest rates” – how Warsh balances Fed credibility with external pressure will be closely watched.

Bottom Line: The first Warsh-led FOMC meeting is unlikely to be about the rate decision itself. Instead, markets will be focused on whether Warsh begins to shift the Fed’s operating framework through less forward guidance, a clearer preference for balance sheet normalization, and a more inflation-first tone in the press conference. The base case is a credibility-building message rather than an immediate policy pivot.