The GSE Bid Cools, Capacity Stays Open

The Rithm Take

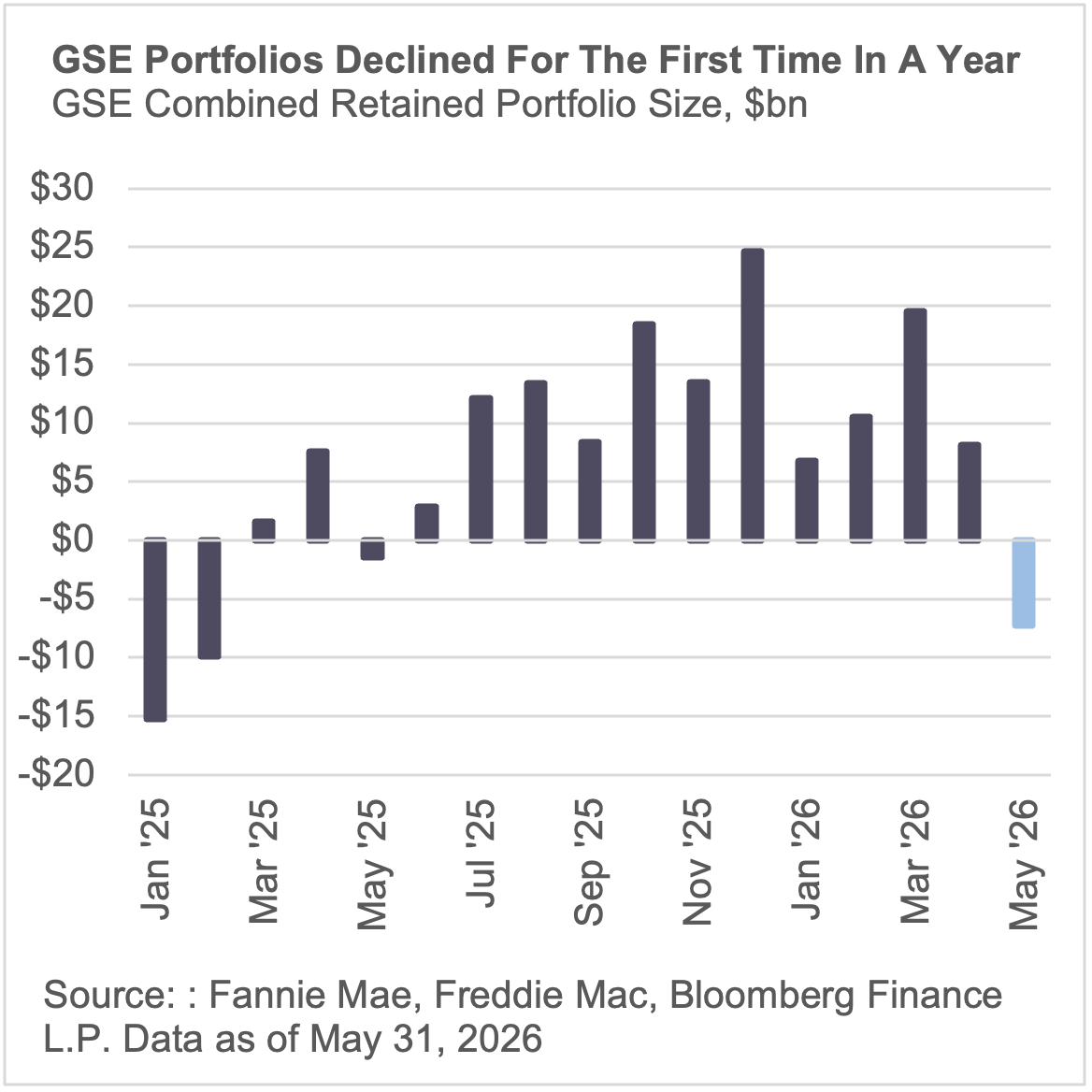

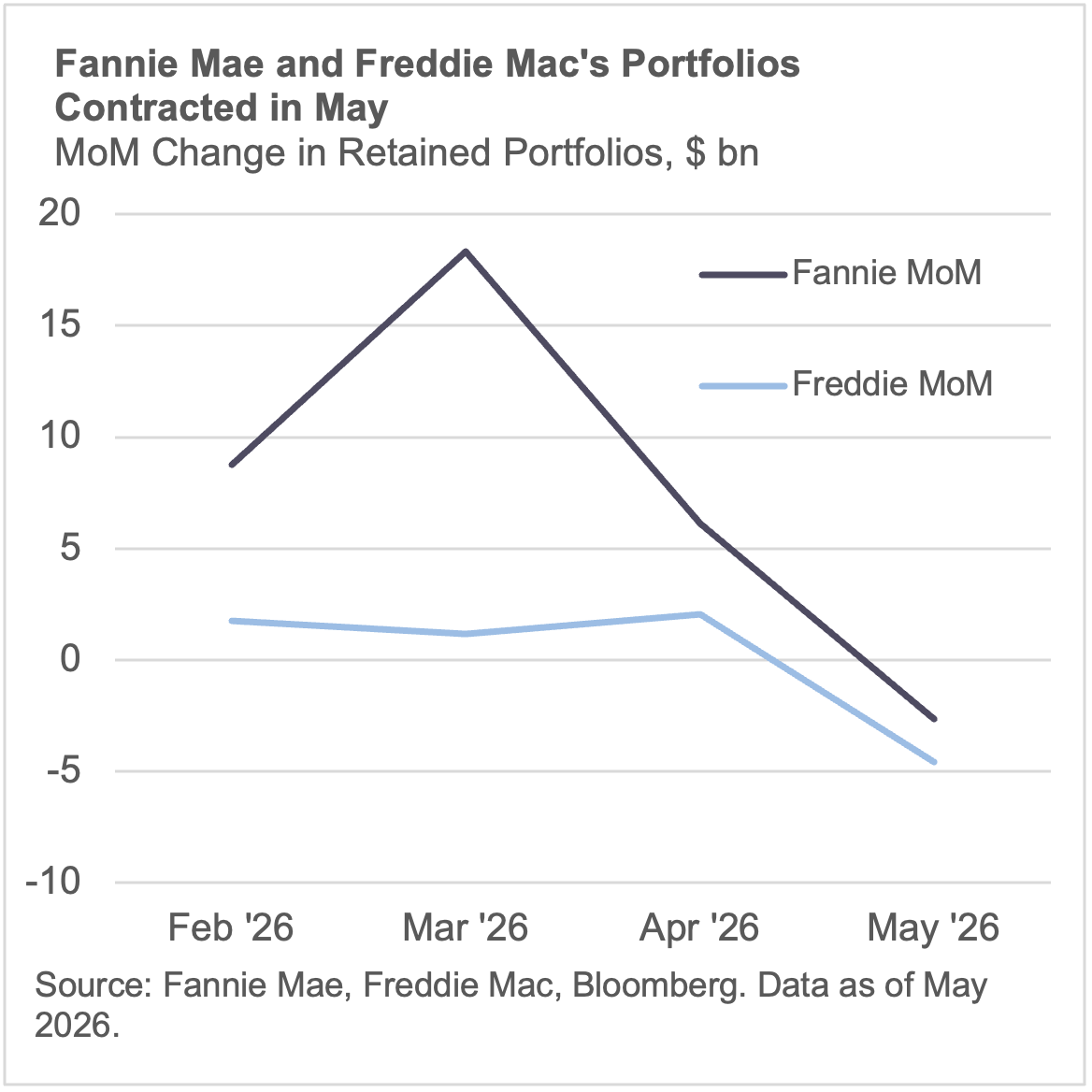

May's combined GSE retained portfolio data shows the first monthly decline since the $200bn buying program was announced early this year. Fannie and Freddie together shed roughly $7.3 billion, with Fannie down $2.7 billion and Freddie down $4.6 billion. Combined holdings now stand at approximately $309 billion, down from April's $317 billion.

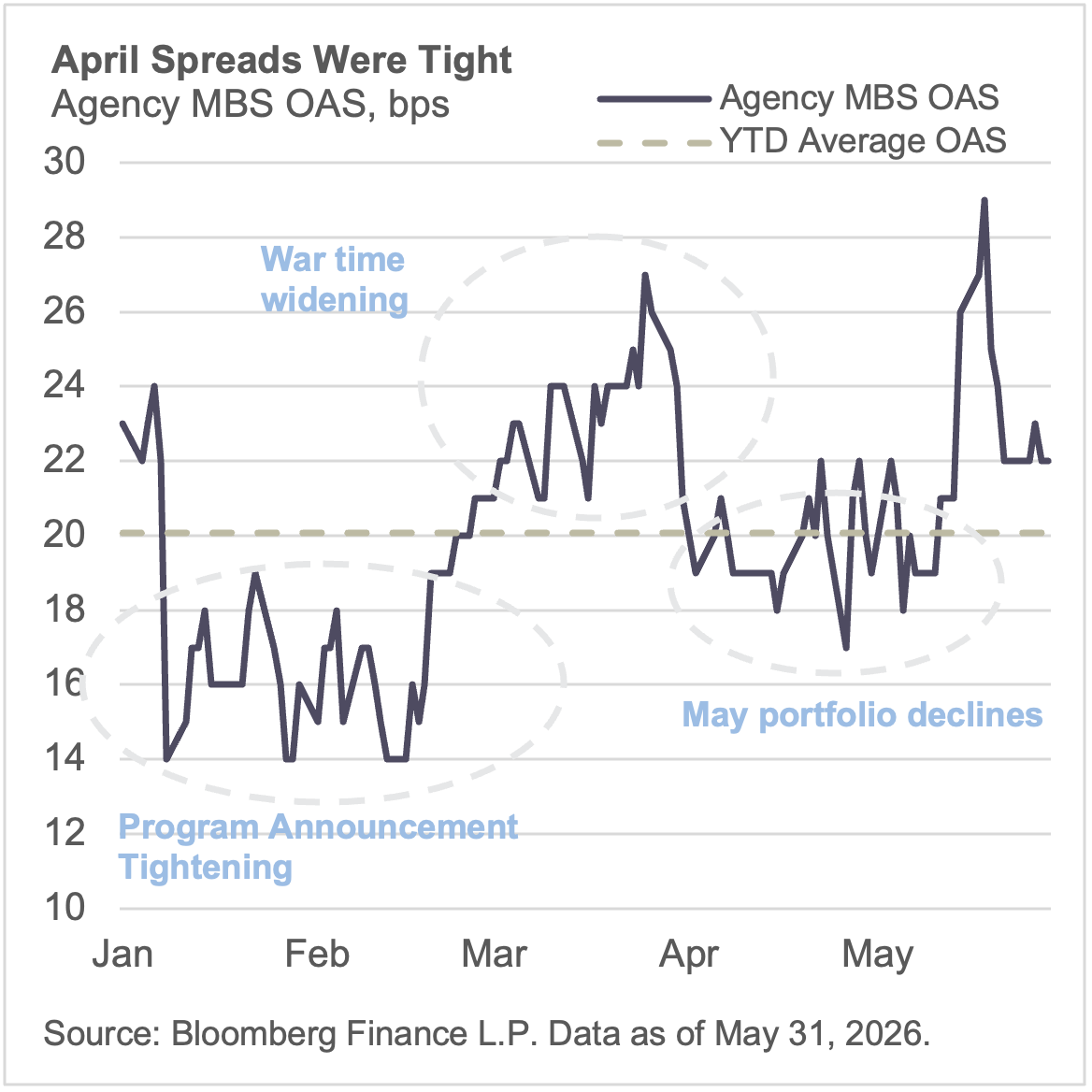

GSE portfolio purchases run through the TBA market, where trades are committed to a coupon, price, and settlement date in advance, with actual settlement occurring the following month. April's agency MBS OAS averaged near 20 basis points on current coupon, and tighter spreads tend to reduce the economic case for buying at scale.

May's OAS has since widened, in line with where the GSEs have historically stepped up purchases. If spreads are the relevant driver, that argues for renewed portfolio growth in the June data rather than continued contraction, though we'd treat that as a thesis to test rather than a settled call.

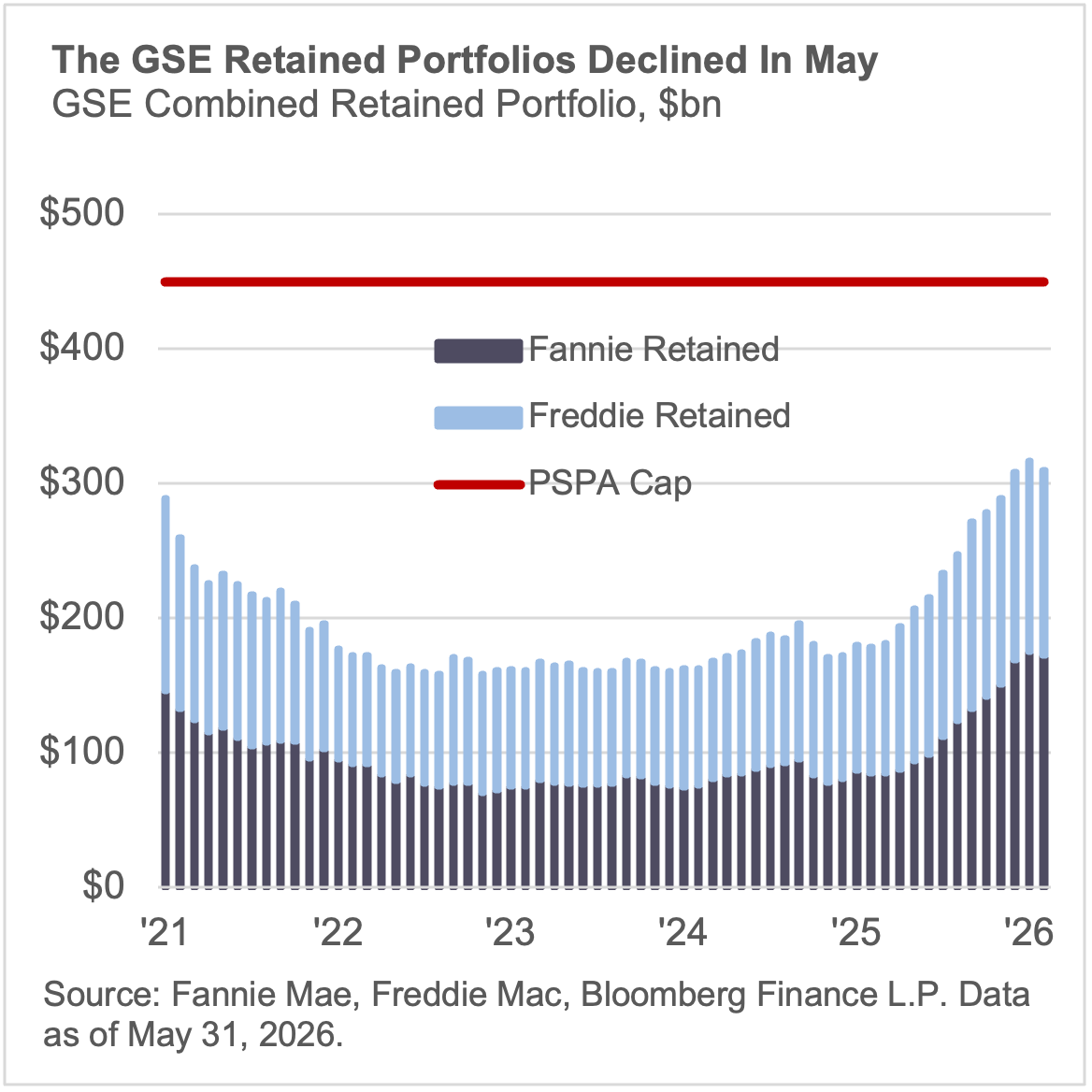

Bottom Line: Our working view is that May's decline looks more like a pause tied to a tighter spread environment than a reversal of the GSE bid, though portfolio decisions are not purely mechanical and other factors could be at play. Spreads have since moved back toward the range where the GSEs have previously shown willingness to buy, which is worth watching in next month's data. Capacity remains ample, with combined portfolios near $309 billion against the $450 billion PSPA cap, so for now we see the constraint on the bid as more economic than structural.

Market Signals

Combined portfolios contracted for the first time in the cycle.

Fannie and Freddie's combined retained portfolio fell to approximately $309 billion in May from $317 billion in April, a decline of $7.3 billion split roughly $2.7 billion at Fannie and $4.6 billion at Freddie. This is the first monthly decline since the buildup began in mid-2025.

Spreads tightened ahead of the pullback.

Current coupon OAS were tighter in April than March, a dynamic that may have reduced the incentive to add to the portfolio at scale. Given how GSE purchases settle, that tightening is a useful lens for thinking about the May data and what may come from the June print.

Spreads have since widened back toward the range we associate with the activation zone.

Current coupon OAS averaged approximately 22 basis points in May, back near levels that have previously coincided with more aggressive GSE buying. If that relationship holds, it would point to renewed portfolio growth ahead, though we'd note this is a single data point and not yet a confirmed pattern.

Fannie remains the larger holder, and both agencies pulled back.

Fannie's retained portfolio stands at roughly $172 billion versus Freddie's $137 billion. Both declined in May, with Freddie's percentage move somewhat larger, which may relate to Freddie's greater exposure to whole-loan and correspondent flow timing relative to Fannie's more securities-heavy book, though we haven't isolated that as the specific driver.

Capacity headroom is intact.

Combined portfolios of approximately $309 billion sit well inside the $450 billion PSPA cap. We don't read the May pullback as a capacity constraint; it looks more like a spread-driven pause, consistent with the economic buyer framework, though we'll continue to monitor whether other factors are contributing.