Economic Buyers: Where the GSE Bid Activates

The Rithm Take

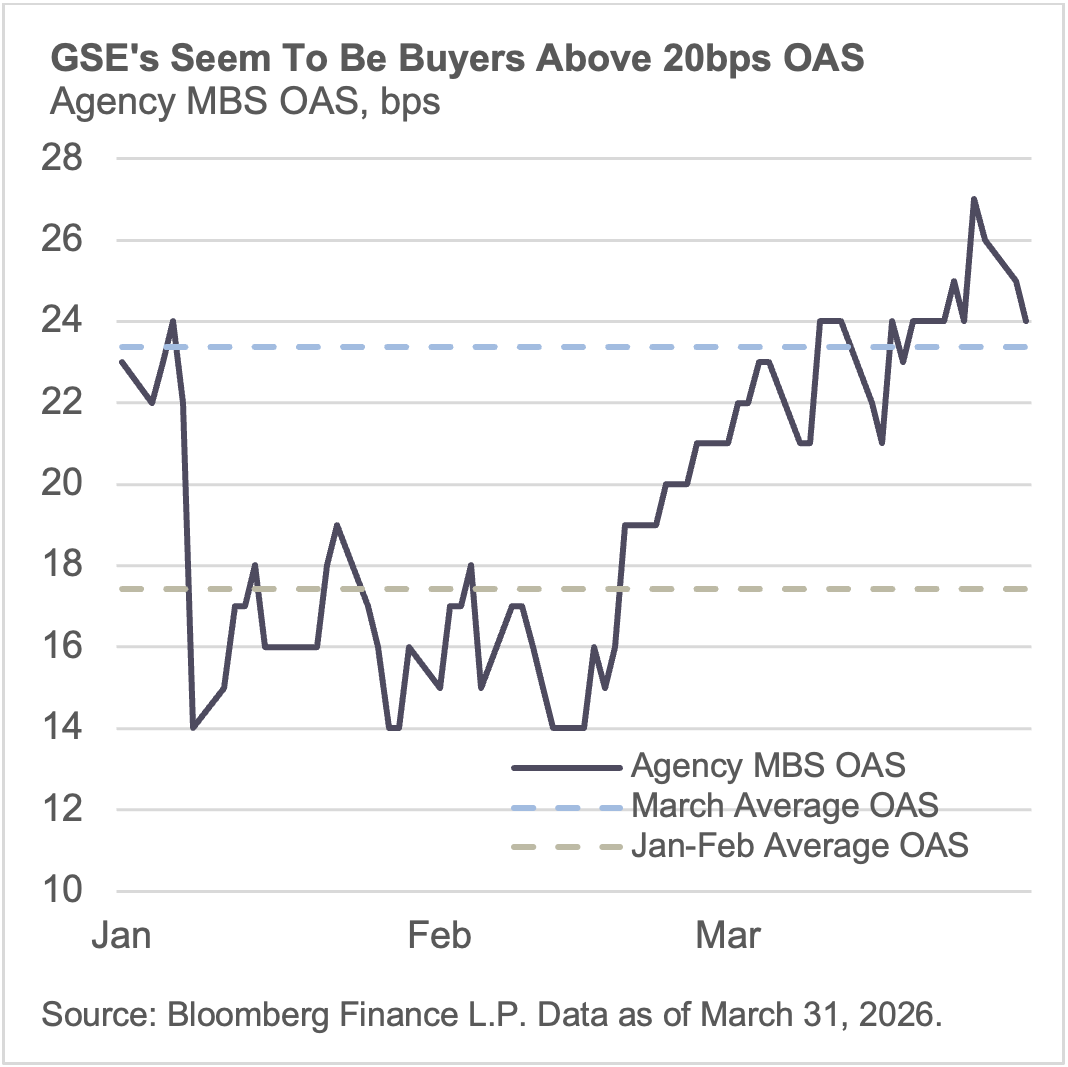

In January, we argued that the GSEs would need to behave as economic buyers with a credible return threshold, not as price-insensitive policy tools. At the time, agency MBS OAS was pricing between 0 and +10 basis points, and we noted that sustained buying at those levels was difficult to reconcile with running the enterprises as economic actors. We expected the bid to show up at wider spreads. It did.

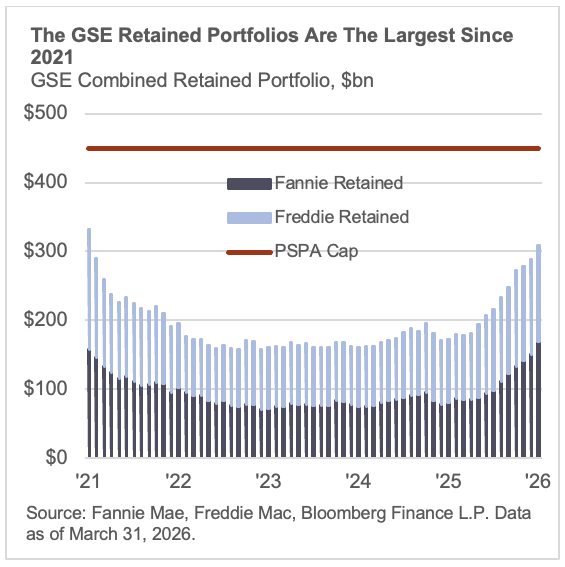

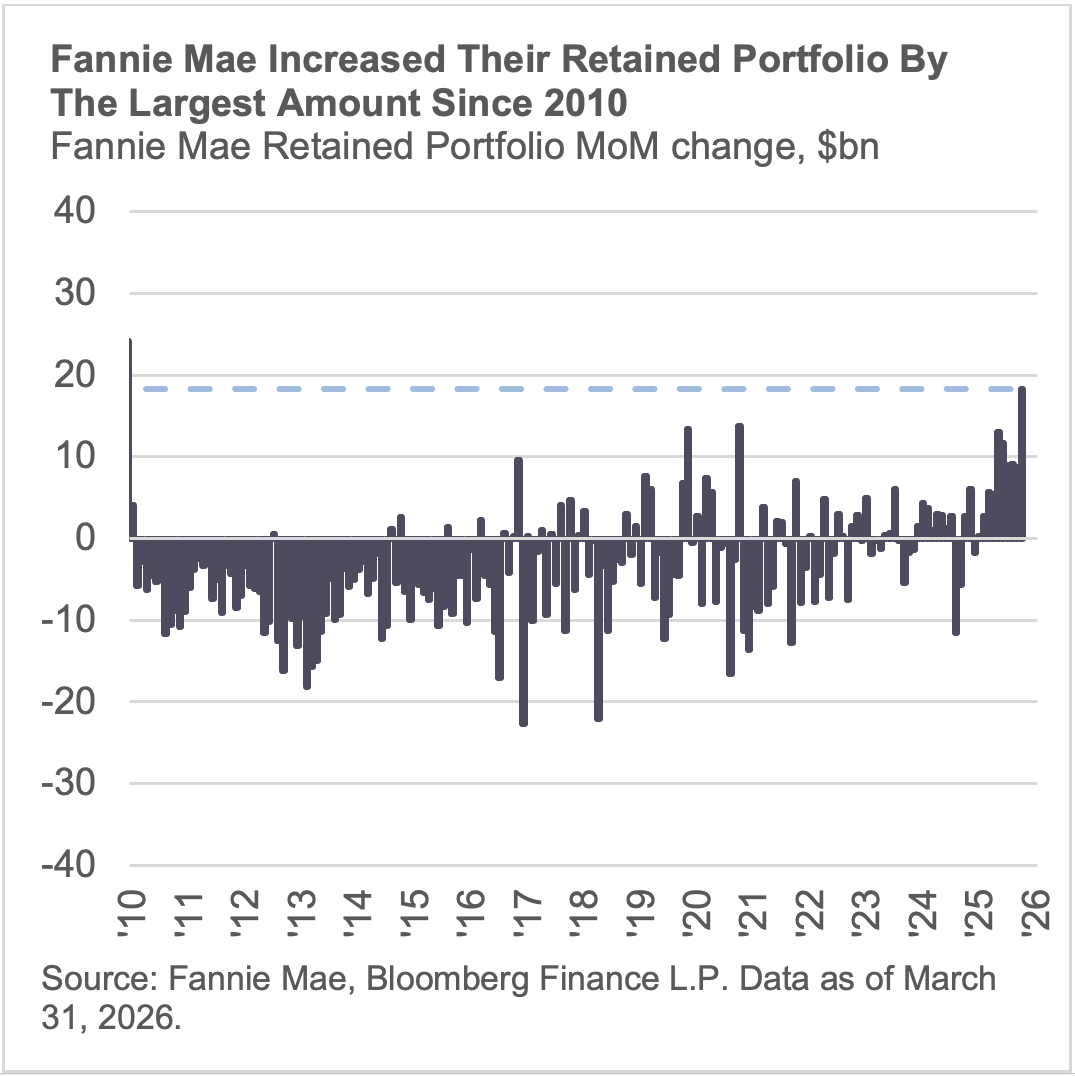

Fannie Mae increased its retained portfolio by approximately $18.3 billion in March, the largest monthly addition since 2009. Combined GSE retained portfolios reached roughly $308.5 billion, the highest level since early 2021. The acceleration coincided with agency MBS OAS widening from an average of approximately 17 basis points in January and February to approximately 23 basis points in March. At 21 basis points today, spreads remain above the level where the GSEs have demonstrated willingness to deploy at scale.

The buying pattern looks economic, not programmatic. When spreads were in the mid-teens, portfolio growth ran at roughly $8-10 billion per month. When OAS moved above 20, the pace nearly doubled. The GSEs appear to be operating with a return hurdle rather than a volume mandate. Spread sensitivity, not calendar-driven allocation, is governing the pace of deployment.

Bottom Line: The GSEs have established themselves as the marginal buyer in agency MBS, and the data now shows where their bid activates. Above 20 OAS, the purchasing pace accelerates. Below it, the pace moderates. That spread sensitivity validates the economic buyer framework and gives the market a reference point it did not have six months ago.

Market Signals

Capacity provides runway, with limits. Under the PSPAs, each enterprise operates under a $225 billion cap. This implies over $100bn of capacity runway. The bid has room to persist, but the program's outer bound is visible.

Fannie added approximately $18.3 billion to its retained portfolio in March – the largest increase since 2010 – a pace not seen since the post-crisis period when the enterprises were absorbing distressed assets under conservatorship. The scale of the current buildup is comparable, but this time is spread-driven purchasing in a functioning market, not crisis-era intervention.

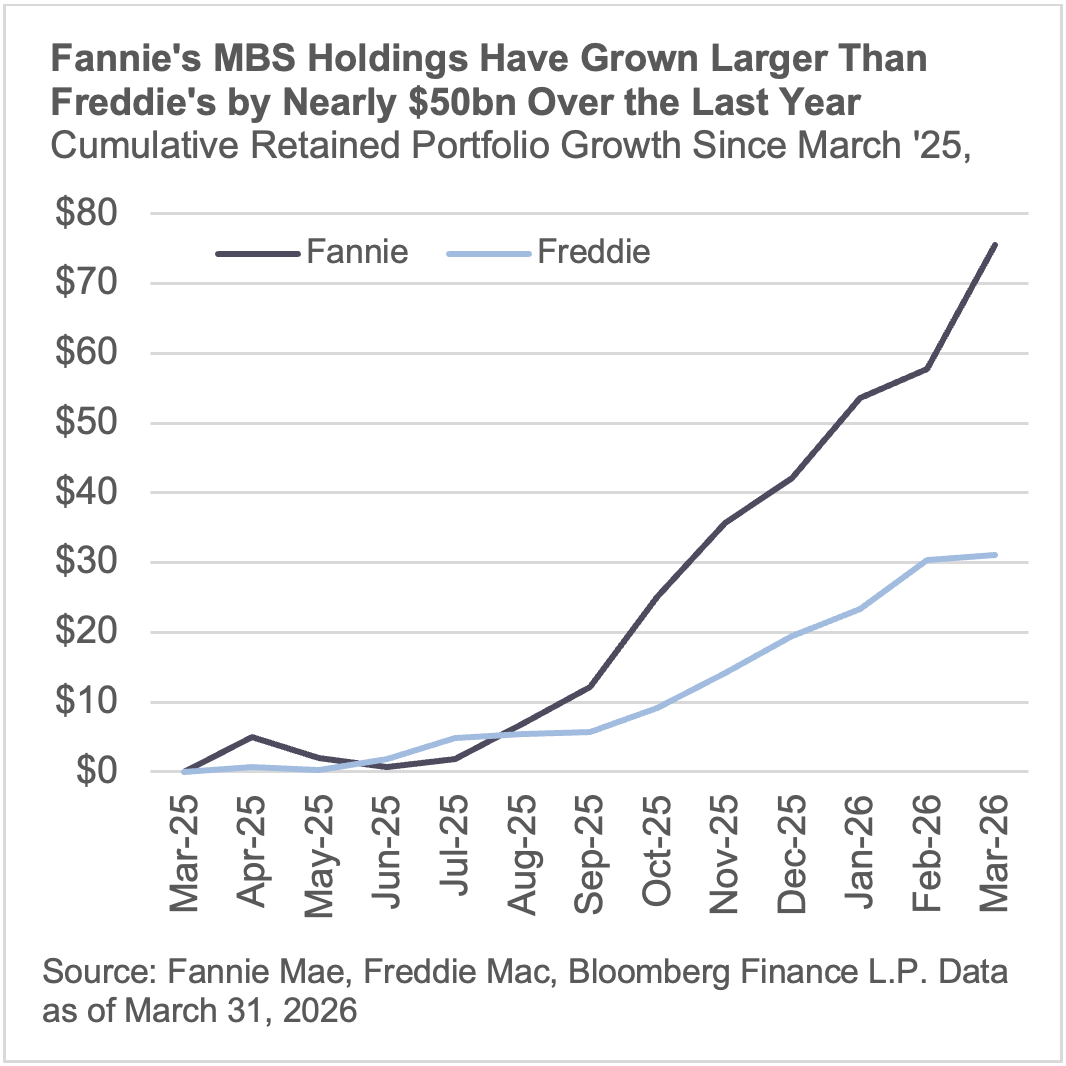

Fannie is leading the MBS buildup. Since March 2025, Fannie has added roughly $75 billion in MBS to its retained portfolio versus approximately $31 billion for Freddie. Beyond what is shown, the composition of the broader portfolios differs: Freddie holds a larger share of whole mortgage loans relative to securities, suggesting growth through correspondent and bulk loan acquisitions alongside its MBS purchases. Fannie's heavier MBS weighting means its buying transmits more directly into secondary market spread compression.

March's average OAS of roughly 23 basis points coincided with the sharpest acceleration in buying. January and February averaged approximately 17 basis points with more moderate growth. At 21 today, spreads remain in the zone where the GSEs have shown willingness to buy.