Q1 Bank Earnings: Reading Between the Lines

The Rithm Take

Bank earnings confirmed the consumer is still performing. Card volumes grew, credit losses improved or held steady, and revenue rose across the majors. JPMorgan released consumer reserves. Bank of America's provision came in below both the prior year and consensus.

But the commentary told a different story than the numbers. Wells Fargo described the consumer as "resilient in the aggregate but increasingly bifurcated beneath the surface." Citigroup skewed its reserve models further toward a downside scenario. JPMorgan's Dimon flagged "an increasingly complex set of risks." The numbers say the consumer is fine. The tone says management teams are proceeding cautiously.

The regulatory backdrop adds a second dimension. The March Basel III re-proposal and the Administration's mortgage executive order are designed to improve the economics of holding mortgage assets on bank balance sheets, broadening the private-sector buyer base for mortgage risk. That supports the Administration's affordability objective and is one of the few levers that can compress borrowing costs at the long end of the curve.

Market Signals

1. Spending held up. The split underneath it is what banks are watching.

Card volumes grew across the majors and consumer banking revenue posted solid year-over-year gains. But the more telling signal came from how banks characterized the strength. Wells Fargo described a consumer that is "resilient in the aggregate but increasingly bifurcated beneath the surface," with higher-income households insulated by asset prices while lower-income cohorts absorb rate and energy pressure with less cushion. JPMorgan noted energy costs remain a modest share of total spend but acknowledged the picture could shift if elevated prices persist into the second half. The question now is if the thinning consumer cushion can persist through the recent market volatility.

2. Credit performance was the positive surprise of the quarter.

The consensus coming in was for gradual deterioration. Instead, loss rates improved or held steady across the group. JPMorgan's card delinquency rate fell year-over-year, Wells Fargo's consumer charge-offs declined, and Bank of America's provision came in roughly $190 million below consensus. Banks are not seeing the stress that the macro narrative would suggest. That does not mean it cannot develop, but it has not shown up in the credit data yet, and the gap between expectation and reality was notable this quarter.

3. Where the group diverges is on what comes next.

Realized credit was clean for the most part, but forward positioning was bifurcated. JPMorgan released $139 million in consumer reserves and its weighted average unemployment assumption actually improved, falling from 5.8% to 5.6%. Bank of America's provision declined year-over-year. Citigroup moved in the opposite direction, building $579 million in net reserves, raising its unemployment assumption from 5.2% to 5.4%, and explicitly skewing further toward a downside scenario near 7%. Wells Fargo sits in between with a modest build and elevated downside weighting. The divergence tells you the uncertainty is concentrated in the forward outlook, and that banks are making different judgments about the same set of risks.

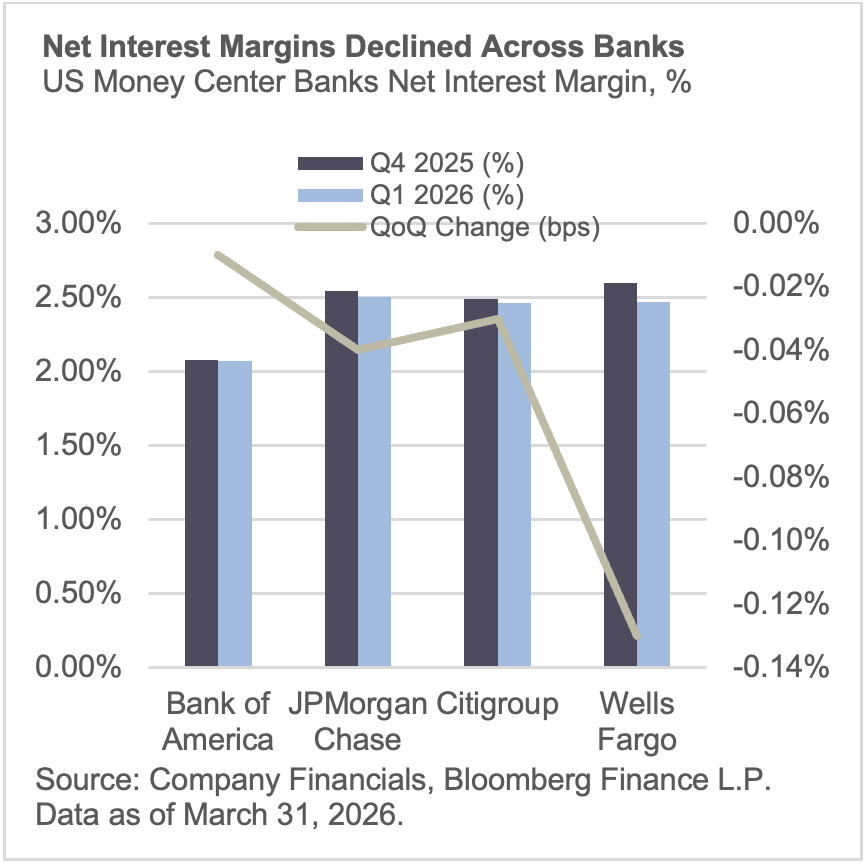

4. Banks are growing revenue by volume, not by earning wider spreads.

NII rose year-over-year at every major bank, but margins compressed across the group as deposit costs stayed elevated and rate cuts worked through the book. Wells Fargo's NIM fell 13 basis points quarter-over-quarter with further compression expected. JPMorgan trimmed its full-year NII guidance by $1.5 billion. The headline growth came from volume, not pricing power. That works when loan demand is healthy and credit stays clean. It leaves less room for error if volume slows while margins are already thin.

5. Mortgage activity is turning, and regulatory relief supports that at the margin.

Bank mortgage portfolios continued to shrink, a trajectory that has been in place for years as post-crisis capital rules made holding and servicing mortgage assets less economic. But originations moved meaningfully higher, with JPMorgan's volume jumping 46% year-over-year. Wells Fargo expects balance declines to moderate and eventually flatten. The regulatory backdrop is shifting in the same direction. The Basel III re-proposal would lower capital charges on residential exposures and ease the treatment of mortgage servicing assets, while the Administration's executive order targets compliance friction for smaller banks. This does not undo the structural reasons banks ceded share. But it broadens the pool of private-sector capital willing to hold mortgage duration, supporting the Administration's affordability objective and putting incremental pressure on spreads.

Bottom Line: The consumer is performing and credit came in better than feared. But management commentary was more cautious than the results, flagging bifurcation, energy drag, and a second half where the cushion thins. NII growth is driven by volume but margin compression is a headwind that bears watching if the revenue environment softens. On the mortgage side, origination activity is turning and the regulatory shift toward lower capital charges could broaden the buyer base for duration and support affordability over the next 12 to 18 months. The near-term story is earnings durability. The medium-term story is to what magnitude regulatory tailwinds can entice banks and the private sector to drive rates lower at the long end of the curve.