No Cut, No Clarity: The Fed Navigates a Deteriorating Tradeoff

The Rithm Take

The FOMC is expected to hold rates steady next week. The decision is not the story. The story is that the Fed is stuck, and the data are making it harder to get unstuck.

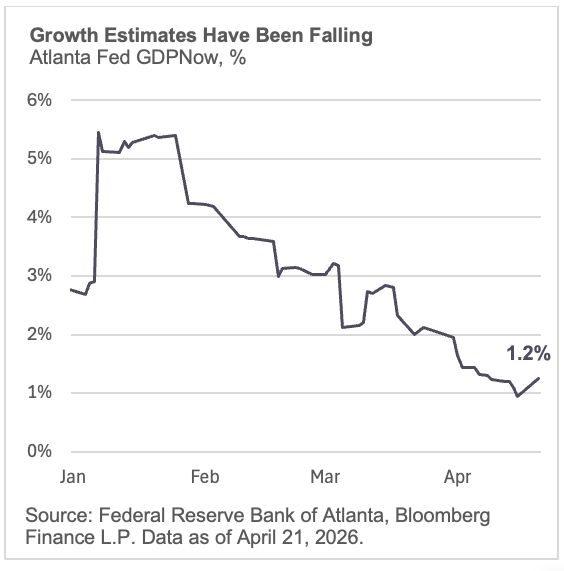

Growth has decelerated sharply. GDPNow has fallen from above 5% at the start of the year to roughly 1.2%. The Committee's own March SEP projected 2.4% GDP growth for 2026; barely five weeks later, the real-time tracking estimate is running at half that pace.

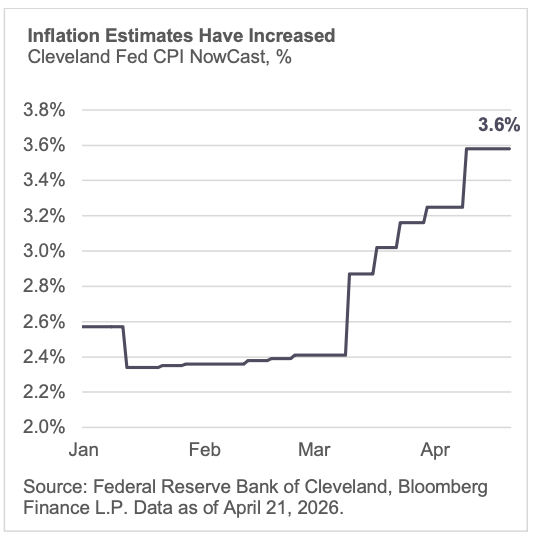

But the Cleveland Fed's inflation nowcast has moved to 3.58%, up from roughly 2.4% earlier in the cycle. The March SEP marked up core PCE to 2.7% for year-end 2026, a significant revision from 2.5% in December. Even that higher forecast now looks like it may understate the problem. Oil prices, elevated since the Iran escalation, are adding a persistent cost channel that risks bleeding from headline energy into core goods and eventually core services through transportation, logistics, and wage bargaining.

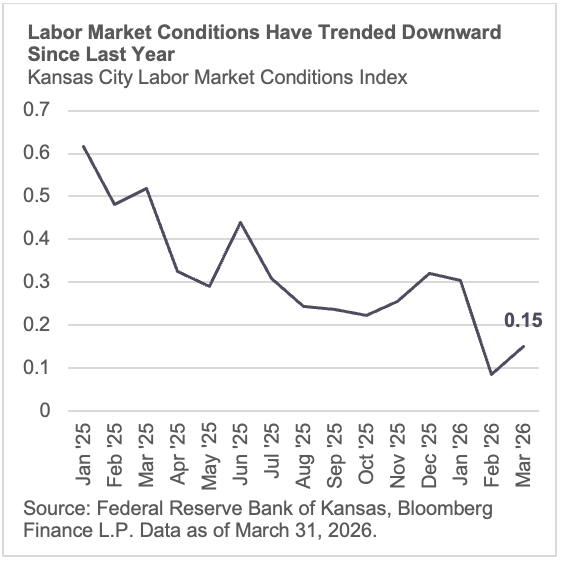

The Kansas City Fed's Labor Market Conditions Index has trended lower for over a year, settling near 0.15 in March. That is cooling, not contraction, but it limits the Fed's ability to lean on employment strength as cover for patience on inflation, even if the low hire/low fire environment is keeping the unemployment rate contained. The March SEP held the unemployment projection steady at 4.4% for Q4 2026, unchanged from December, even as the risk diffusion index showed 84% of participants weighted unemployment risks to the upside. Both sides of the mandate are binding simultaneously, and the Iran-driven supply shock is the kind of problem monetary policy cannot address without accepting weaker growth.

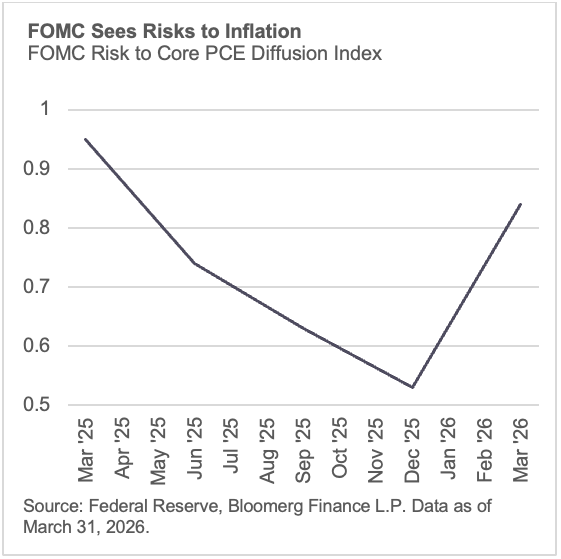

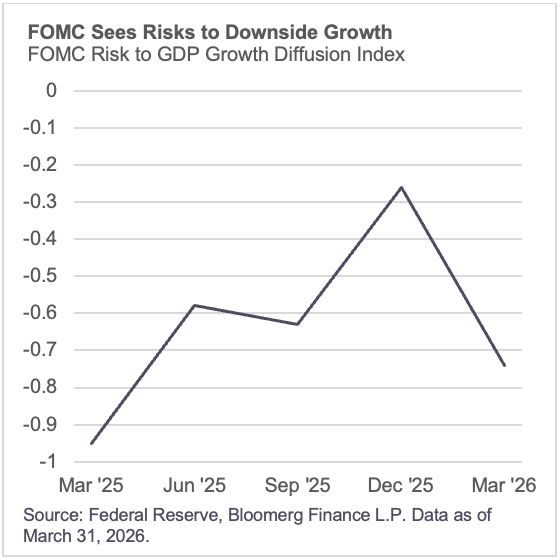

The Committee itself sees the risks as asymmetric. In the March SEP, 84% of participants flagged upside risks to inflation, 74% flagged downside risks to growth, and 84% flagged upside risks to unemployment. That is nearly the entire Committee positioning for stagflationary outcomes, and it preceded the worst of the oil shock.

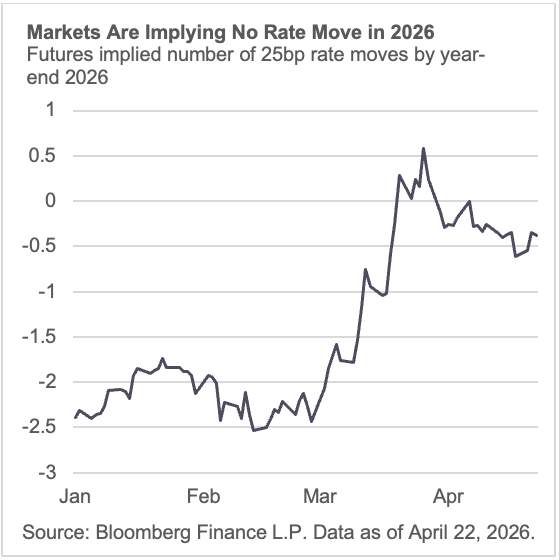

Markets entered the year pricing more than two cuts by December. That has collapsed to less than half a cut. The repricing accelerated through late March and April alongside the oil shock. Markets are no longer debating the pace of easing. They are debating whether easing happens at all this year. The March SEP median still implied one cut in 2026, bringing the funds rate to 3.4%. Futures are now pricing just a ~30% chance of a cut in 2026.

Bottom Line: The window for easing has narrowed. Growth is decelerating, inflation is reaccelerating, and the oil shock adds a cost channel monetary policy cannot easily offset. The March SEP projections, just five weeks old, already look stale on both growth and inflation. The direction is higher for longer on rates.

Market Signals

Growth and inflation are diverging. GDPNow at 1.2% and the Cleveland Fed inflation Nowcast at 3.58% capture the bind: the economy is slowing into an inflation problem, not out of one. The March SEP projected 2.4% growth and 2.7% core PCE for 2026. Both are already being challenged in the wrong direction.

The Fed path has been repriced. From more than two implied cuts to less than half a cut since January. The SEP median still penciled in one cut this year. The market has moved past it.

The Committee's own risk assessment is skewed. Diffusion indices from the March SEP show 84% of participants flagging upside risks to inflation and unemployment, with 74% flagging downside risks to growth. That is a stagflationary distribution, and it preceded the worst of the oil price passthrough.

Labor is softening, not breaking. The KC Fed index near 0.15 is consistent with labor market pressure.