Consumers in Flux as the Cycle Turns

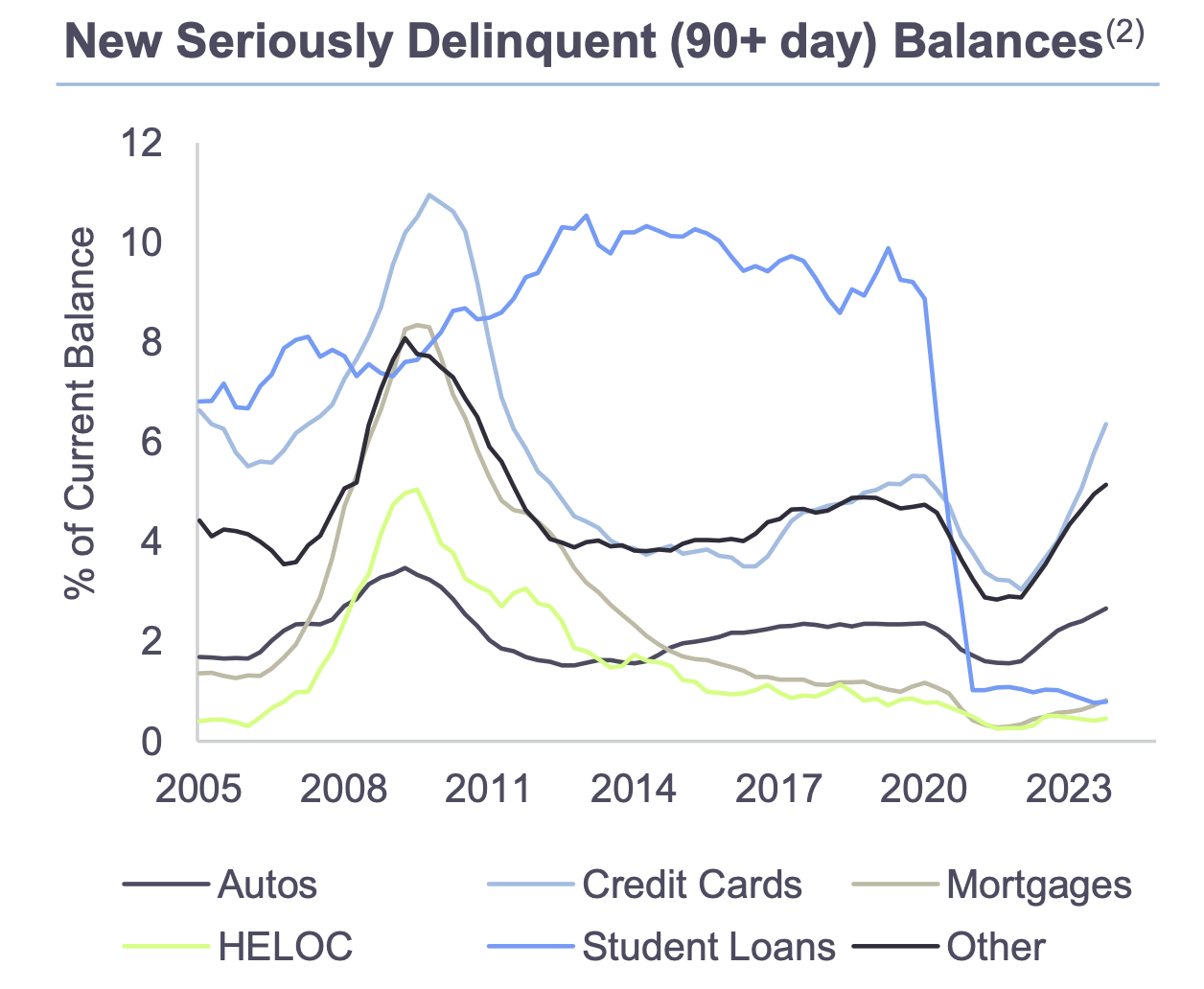

The New York Federal Reserve’s Quarterly Report on Household Debt and Credit is showing signs of consumer stress. Specifically, new seriously delinquent (90+ day) loan balances on autos and credit cards are well above the levels reported prior to the pandemic despite today’s stronger job market.

The Conversation

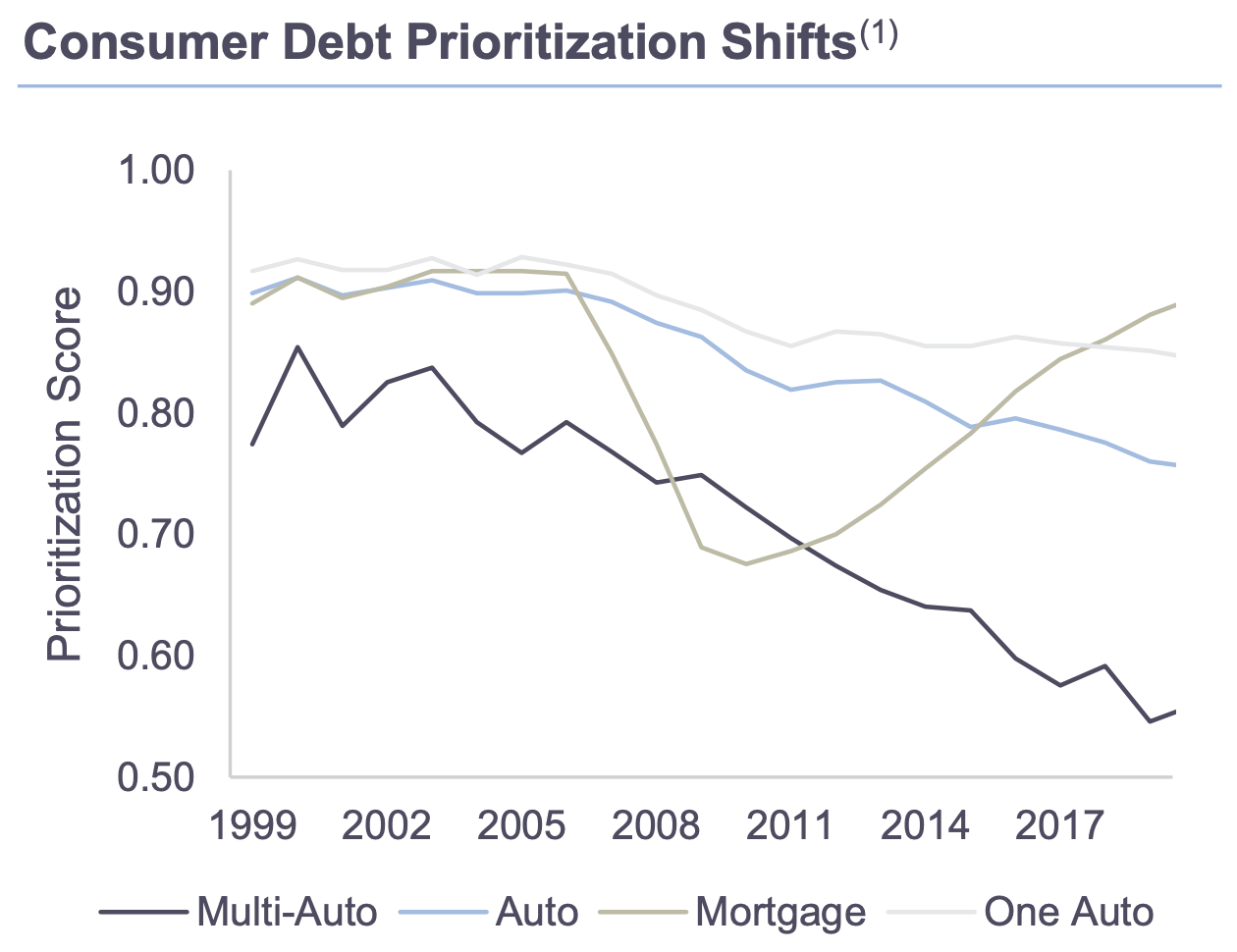

Consumer debt prioritization decisions change across credit cycles. During the post-GFC period, consumers’ prioritization on mortgage payments has risen while the priority of auto loan payments has slid for those owning multiple vehicles. This prioritization ladder is affirmed in the latest report from the New York Federal Reserve showing rising delinquencies on autos and credit cards.

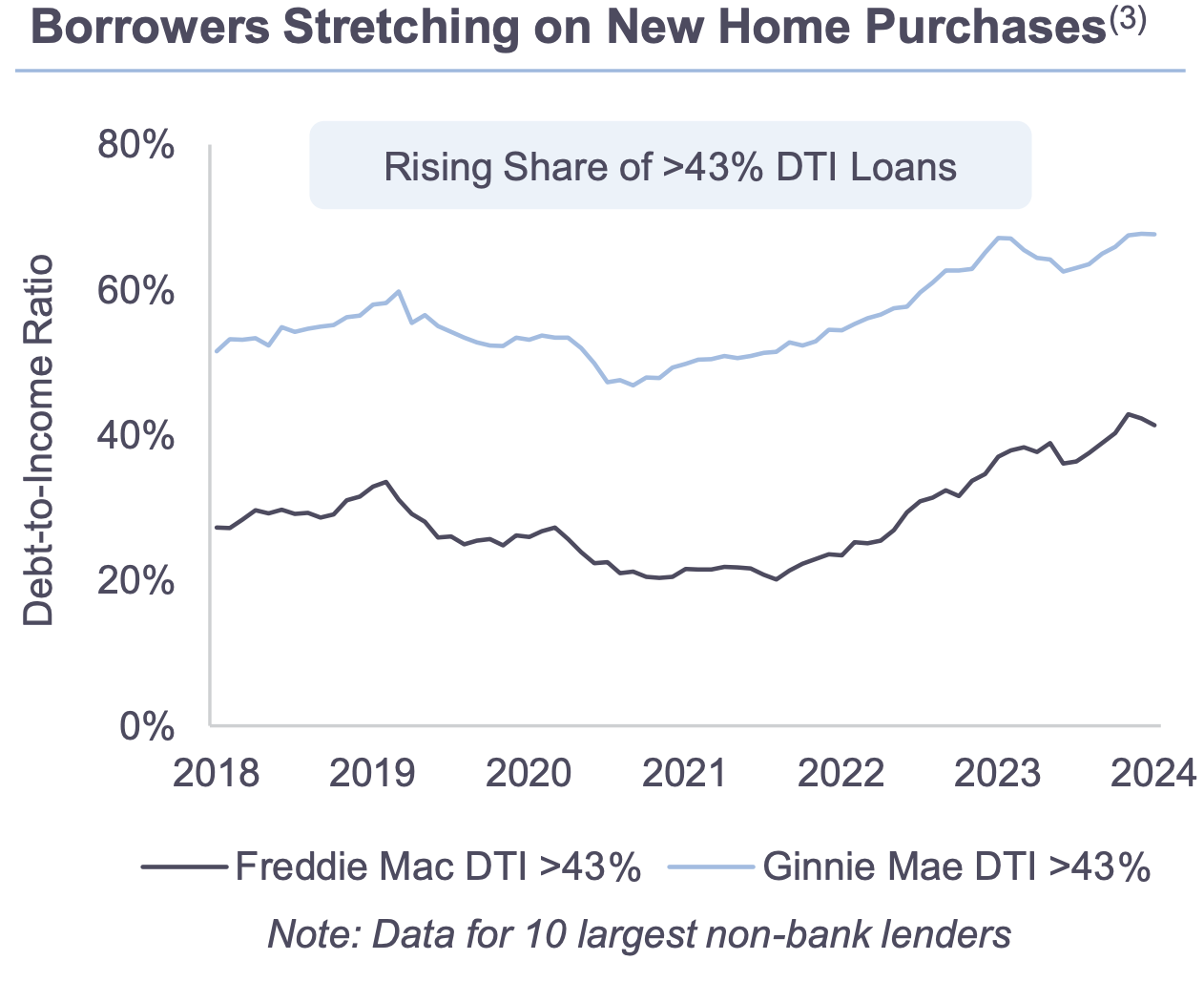

Consumer debt loads have shifted through the 2022-2023 high rate environment. For instance, new homebuyers are stretching to afford the purchase of a home. Since late 2021, debt-to-income (DTI) ratios have steadily risen across high and low credit borrowers with rising shares of high DTI borrowers (>43% DTI).

The outlook for consumer performance is strongly dependent on continued labor market strength. Consumers have worked off pandemic era excess savings. Consumers are also spending a high share of their disposable income, driving down the personal savings rate.

The Rithm Take

Consumer credit score inflation is broadly evident, with 2022 and 2023 high credit score borrowers performing as weak as lower credit score borrowers pre-pandemic. Layered risk comes from this, total debt loads (irrespective of credit score) and lender underwriting standards, which is all factoring in to increased delinquencies. This affects recent vintages of a variety of consumer credit lines, from mortgages to unsecured lines of credit.