The GSE Bid May Have A Price

The Rithm Take

The market pricing GSE’s as a policy tool is in flux.

The January GSE (Fannie Mae and Freddie Mac) retained portfolio numbers are in, which is the first real data point since the $200 billion purchase program announcement. When we wrote about this program in January, the central argument was that the initial spread tightening reflected a one-time flow shock, not the beginning of a durable, price-insensitive demand regime. The January data reinforces that view and sharpens the question that now matters most: what kind of buyer are the GSEs going to be?

The distinction is not semantic. A non-economic buyer — one purchasing to drive affordability regardless of spread levels — produces a different market outcome than an economic buyer with a return threshold and a clearing option adjusted spread (OAS). The former is a persistent tightening force. The latter is a backstop. The January numbers, read alongside the annual report disclosures, suggest the GSEs are trending toward the latter. The basis has largely priced the former. That gap is where the risk lives.

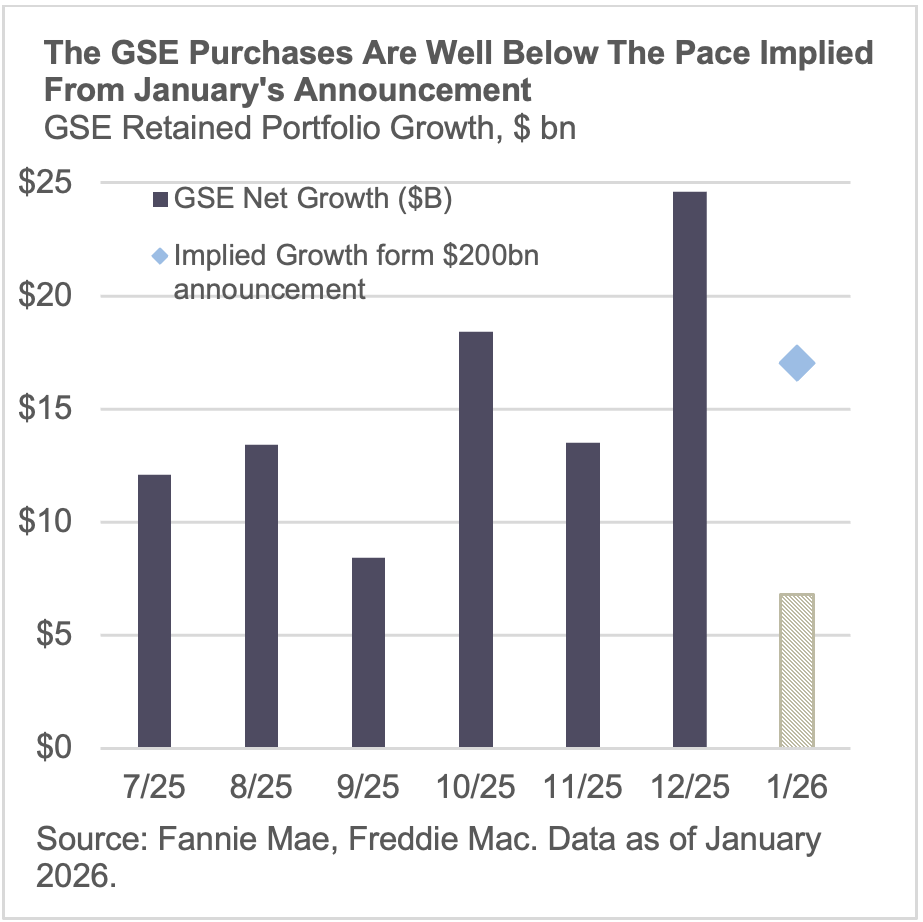

1. January's purchase pace was underwhelming relative to the program's implied run rate.

To execute $200 billion in purchases over a calendar year, the GSEs would need to average roughly $17 billion per month. January's combined net portfolio growth was approximately $6.7 billion — Fannie added a net $9.1 billion while Freddie declined -$2.4 billion. That is less than 40% of the monthly pace required. One month does not make a trend, but it is not the pace of an entity buying with urgency. It is the pace of an entity that is selective.

2. The PSPA cap is the binding constraint and it has not been amended.

The existing $225 billion portfolio cap was not revised alongside the program announcement. Combined remaining capacity across Fannie and Freddie is ~$150bn, meaningfully less than $200 billion announcement. At the $17 billion monthly pace the program implies, the GSEs would hit the cap well before year end. Without a revision, the program cannot be fully executed as announced. While amending the cap is a fairly straightforward agreement between Treasury and FHFA, it remains a step to be completed.

3. Future purchases will increasingly rely on debt funding.

Early GSE purchases were funded primarily from existing cash reserves. That liquidity has been largely deployed. Going forward, purchases will be funded through a mix of cash from operations and debt issuance. A buyer with a cost of funds is more likely to be price-sensitive than one drawing from a liquidity buffer — which is worth monitoring as the program progresses and OAS remains compressed. This is less a near-term concern and more a question that sharpens as the GSEs approach the back half of the $200 billion program.

4. The GSEs are behaving like economic buyers, not the Fed.

QE worked because it combined three features: indefinite duration, total price insensitivity, and reserve creation that pulled banks into the bid. None of those apply here. The GSEs are not buying on a schedule, not committed to any particular coupon, and not operating without a balance sheet constraint. Roll specialness surged (buyers competing for near-term delivery of mortgage securities) after the announcement and has since normalized, which is consistent with a market that has repriced from a “QE-like” scenario.

5. Where do GSEs become economic buyers?

The GSEs have signaled they will be likely to increase purchase activity when spreads widen and pull back when spreads are tight. Current coupon OAS is near historically tight levels, which may itself help explain January's underwhelming pace. Finding the OAS level at which the GSEs become consistent, motivated buyers is the most important variable for the mortgage basis going forward.