The Consumer Cushion Gets Thinner

The Rithm Take

The oil shock is a regressive tax. The OBBBA benefit is a progressive transfer in reverse. The two are arriving simultaneously and landing on different households. At the aggregate level, they roughly offset. At the household level, for the cohort most exposed to energy costs and least likely to see meaningful tax relief, the net effect is a real income squeeze arriving into a labor market that was already losing momentum before a single missile was fired.

The consumer is not breaking. But the divergence dynamic is widening, and the businesses most dependent on lower-income, high-frequency spending are now facing compounding pressure from three directions at once: energy costs, a labor market where entry-level hiring has slowed, and a sentiment picture where the forward view is deteriorating as current conditions hold.

Market Signals

1. The confidence headline masked a forward view that is deteriorating.

The Conference Board's index edged up to 91.8 in March, beating a consensus of 87.8. The present situation improved. But the Expectations Index fell to 70.9, its 13th consecutive month below 80, the level that has historically preceded recession within a year. What consumers think about right now looks manageable, but what they think is coming is not.

2. The labor market's problem is not layoffs. It is the absence of movement.

JOLTS showed job openings at 6.88 million in February, hires at their weakest outside the pandemic since 2011, and quits at their lowest since 2020. The low-quit read means workers are staying in jobs they would otherwise leave because they do not believe the market will absorb them. That is a labor market where mobility has slowed. When mobility slows, household income formation softens and the natural buffer that absorbs negative shocks disappears.

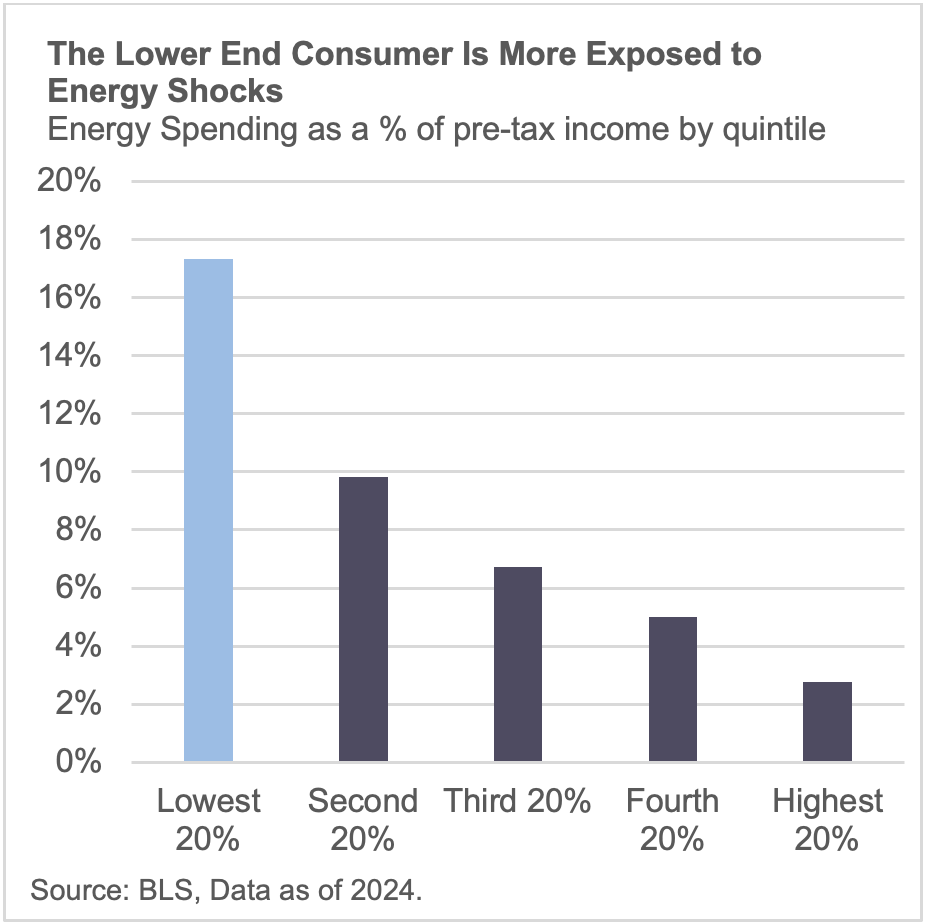

3. The oil shock and the tax cut are not a wash. They are a transfer.

WTI has moved from $71 at the start of March to over $100, a roughly $50 to $75 per month increase in household energy costs at current prices. The OBBBA benefit, running well below its expected pace with cumulative refunds only $23 billion above last year through late March, is skewed toward higher-income earners who spend the smallest share of income on energy. The bottom quintile faces the largest proportional energy cost increase and receives the least fiscal relief. These forces are not netting to zero across the income distribution.

4. Balance sheets are still strong, but the oil shock is eroding the cushion.

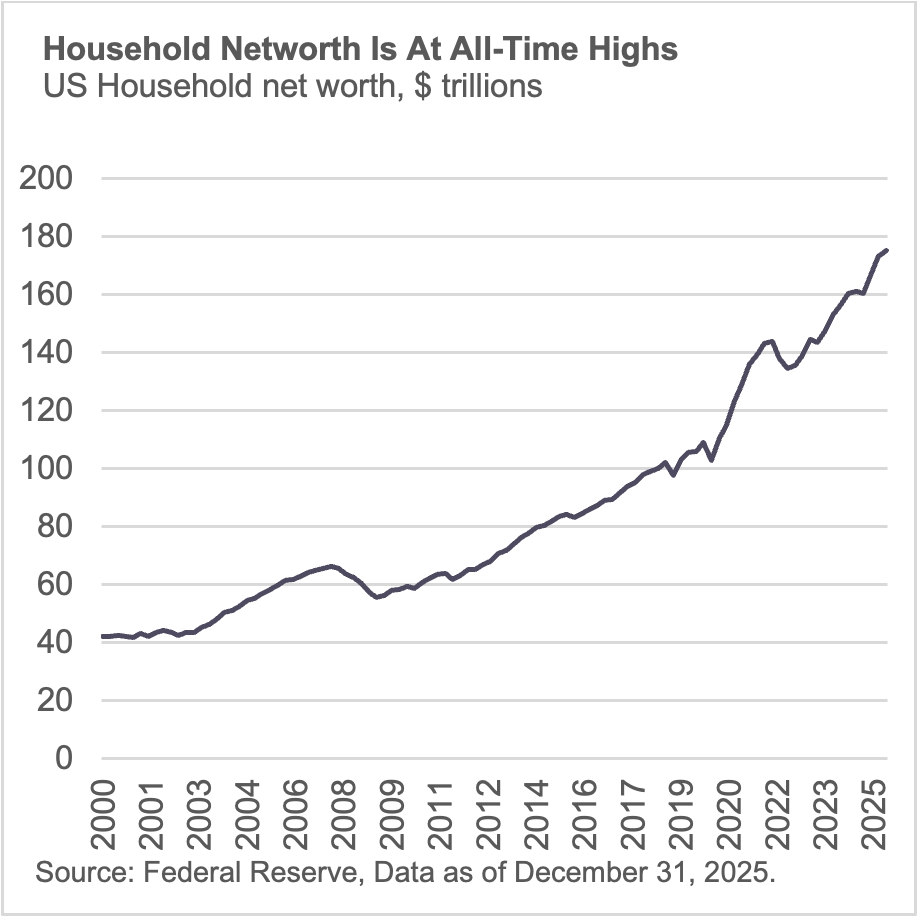

Household net worth remains near all-time highs at ~$180 trillion, the personal saving rate sits at 4.5%, and Fed Governor Barkin noted this week that firms and consumers are not yet acting as though they expect lasting effects from the oil shock.

The risk is that it reflects a lag, not a floor. The S&P 500 declined over 5% in March, eroding roughly $3 trillion in equity value. Oil at $100 is a persistent drag on real incomes. Balance sheet strength can absorb for a limited time, not indefinitely. The cushion exists, but is getting thinner.

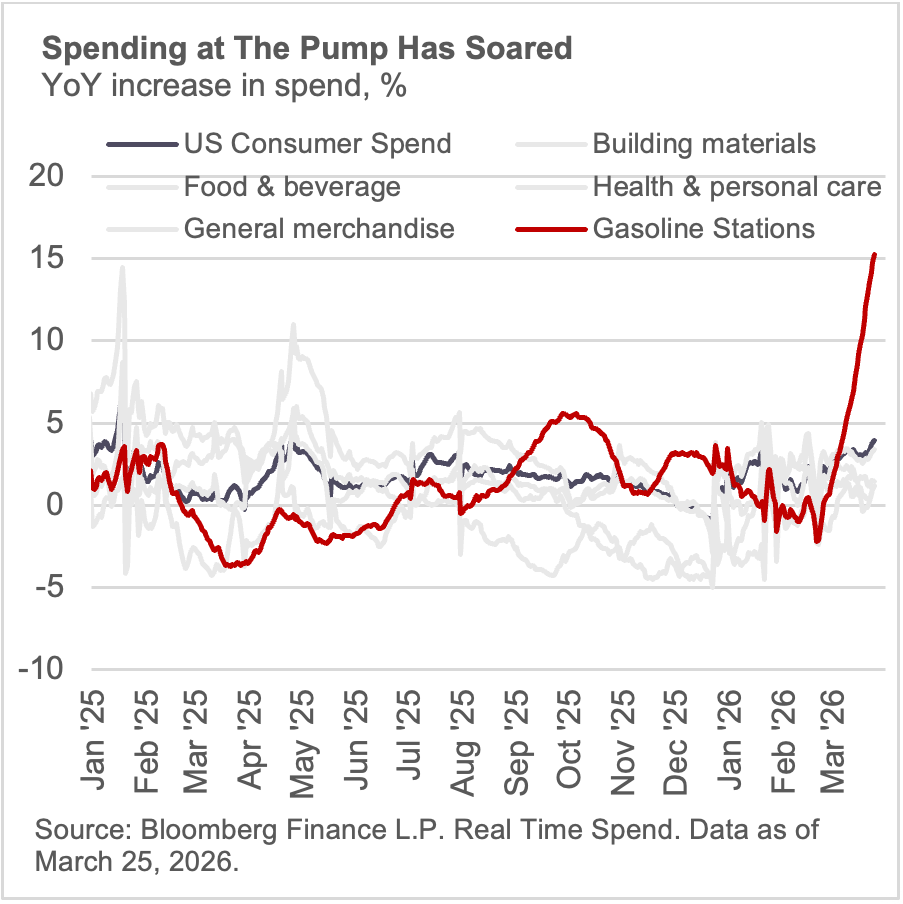

5. Real-time spending shows momentum, but the composition tells the story.

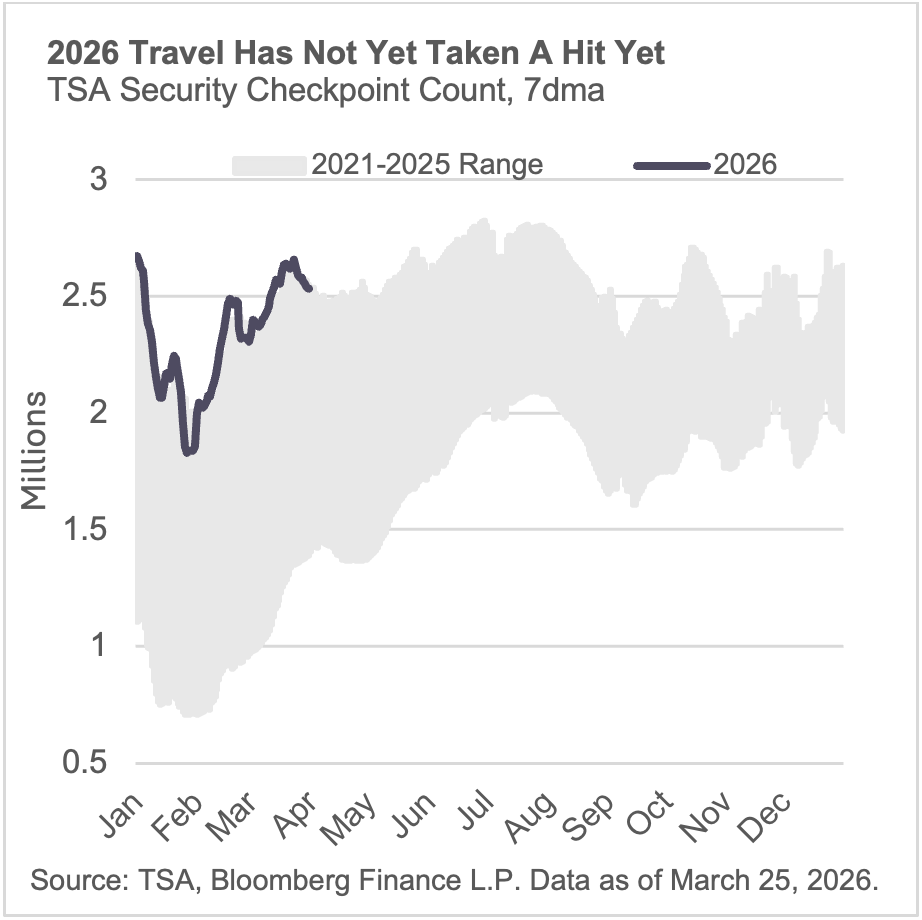

February retail sales rose 0.6% month-over-month, above consensus, with 10 of 13 categories posting gains. Real-time data through late March reinforces that picture at the headline level, with total spending running nearly 4% above year-ago levels and broad-based momentum. Gasoline station spending is up over 15% year-over-year, reflecting price rather than volume. Spending at the pump is crowding out discretionary allocation in real terms for lower-income households even as the aggregate holds. The March print will be the first read that captures whether the categories currently showing momentum can sustain it once the energy drag begins compressing the budgets supporting them. We’ll be looking to discretionary items (air travel, auto purchases, large ticket appliances) to crack first amid a change in consumer behavior.

Bottom Line: The data so far reflects a consumer who entered the conflict in better shape than expected. Retail sales beat, balance sheets are intact, and real-time spending shows rising momentum across several categories. That resilience is real and should not be dismissed. But the leading indicators are pointing in one direction: sentiment on the future is deteriorating, labor market mobility has seized, and the oil shock is landing hardest on the households with the least buffer. The three places to watch for the first signs of a genuine turn are gasoline station spend relative to other categories in real-time tracking data, air travel and accommodation bookings as a read on whether discretionary confidence is holding, and food services and drinking places, the category most sensitive to lower-income pullback and the one that historically softens first when the squeeze becomes real. The conflict's duration remains the primary variable.