Riding the Bull Steepener: How a Diverging Market Helps Financial and Real Estate Sectors

The Rithm Take

A bull steepener is a significant dynamic in the current market, driven by a fundamental divergence between the Fed's "higher-for-longer" stance and the bond market's anticipation of future rate cuts. This steepening of the yield curve—where short-term rates decline due to expected cuts while long-term rates hold steady because of fiscal pressures and a rising term premium—creates a favorable environment for certain sectors. This environment directly benefits financials and various forms of real estate.

Market Signals

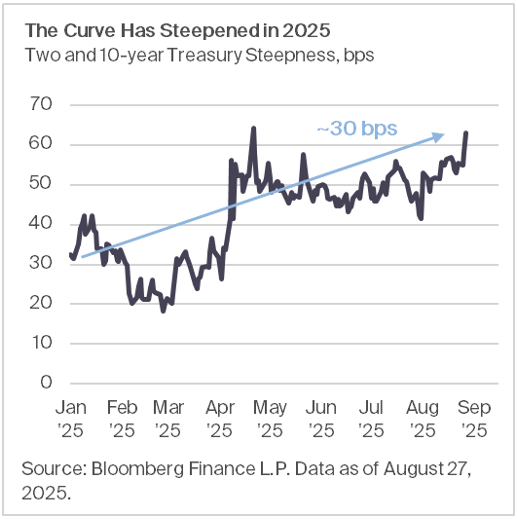

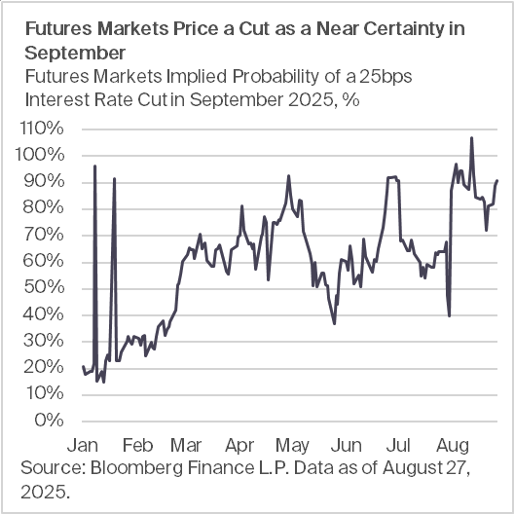

Year-to-date, the two and 10-year curve has steepened by ~30bps, as futures place the probability of a September interest rate cut as a near certainty.

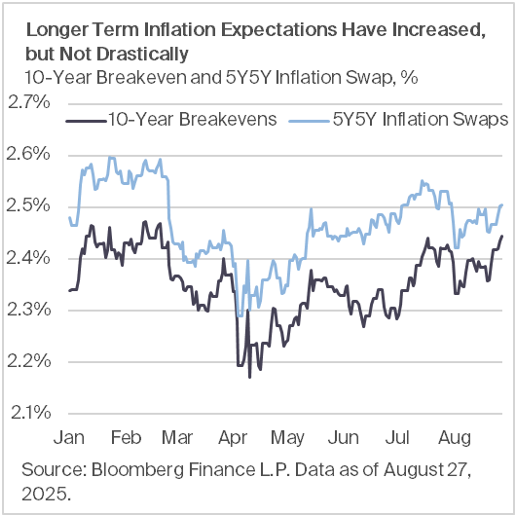

Longer-term market inflation expectations have risen but don't show signs yet of de-anchoring. Both the 5y5y inflation swaps and 10-year breakevens are lower than their levels in February.

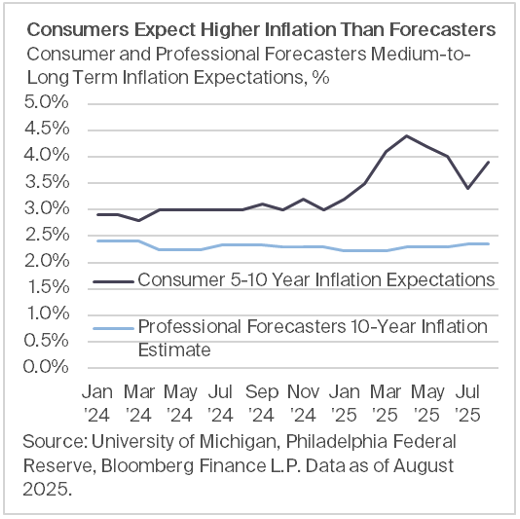

Professional forecasters' expectations for consumer prices over the long run also remain muted. However, consumer expectations, which tend to be more volatile, have shown a marked increase and at 3.9% is nearly twice the Fed's target.

The Conversation

The Treasury yield curve is one of the most closely watched measures in the world of finance and is affected by various factors to a different degree across the curve. The front end is predominantly affected by changes in the overnight rate and Fed decisions, whereas the long end is primarily driven by growth and inflation expectations.

Post-Powell’s speech at Jackson Hole which featured the statement “With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance,” futures markets rushed to increase the probability of a rate cut. Market pricing went from ~65% to ~93%, and while those probabilities have been pared back to around 90% today, money market participants are confident that September will bring a 25bp interest rate cut.

At the same time, fiscal deficits and risks to the Fed’s independence have been rising. President Trump has already replaced Governor Kugler after her resignation with Miran, who is perceived as to be more inclined towards rate cuts. Trump has publicly announced the firing of Governor Cook, though the decision is likely to be contested. This question of independence has consequences for the long end of the curve and adds term premium (extra compensation investors demand for holding a longer-term bond instead of a series of shorter-term bonds for the same investment horizon) to yields. Term premium on the 10-year as estimated by the Fed now stands at roughly 50bps versus about 10bps at this time last year.

All else equal, these dynamics net out to a steeper yield curve, which can be a net positive for financials and various real estate sectors whose liabilities (repo financing) rest at the short end and assets (securities) sit on the long end.