“Passive Tightening” Ahead + Recession Calls Get Reset

Policy in Transition, from Active to Passive Tightening

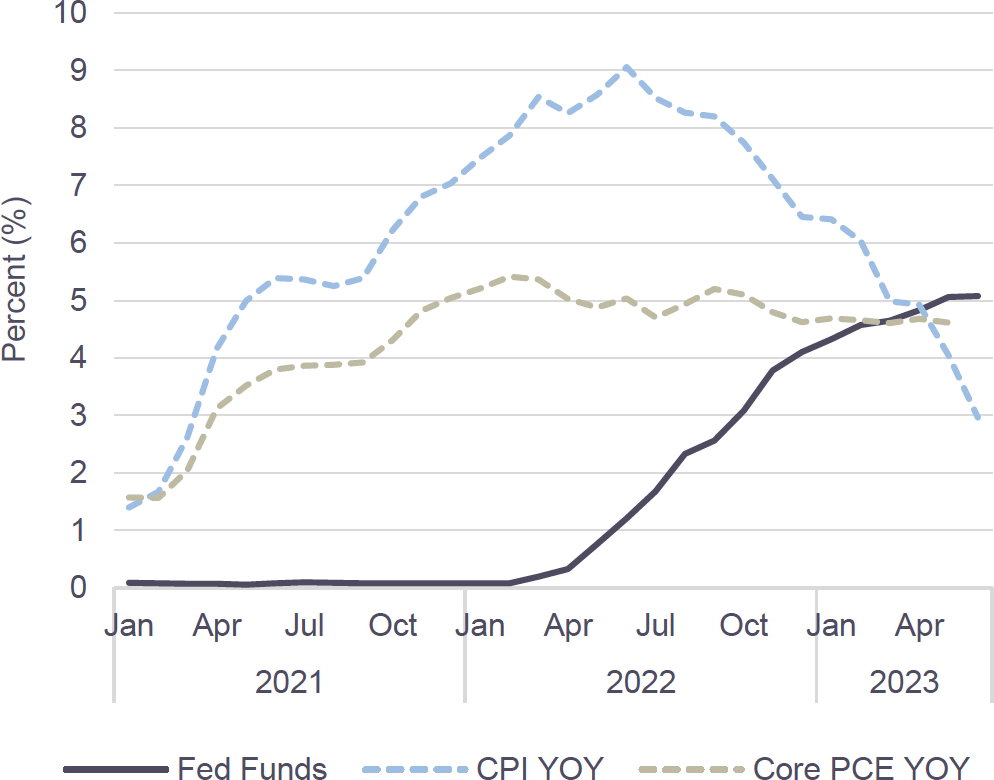

Approaching peak policy rates (even if the Federal Reserve stays on hold) will lead to continued monetary tightening, especially as inflation continues to cool. The Fed has raised policy rates since March 2022, catching up to reported inflation. But cooling inflation today is dropping to levels below policy rates. We believe that if inflation continues to drop, policy will continue to tighten, even if just passively.

Headline CPI inflation, reported at 3%, is down from a cycle peak of 9% in Jun ’22. Similarly, core PCE is at 4.6%, down from a cycle peak of 5.4% in Feb ’22. Both metrics are now below the Fed Funds target of 5-5.25% for policy rates.

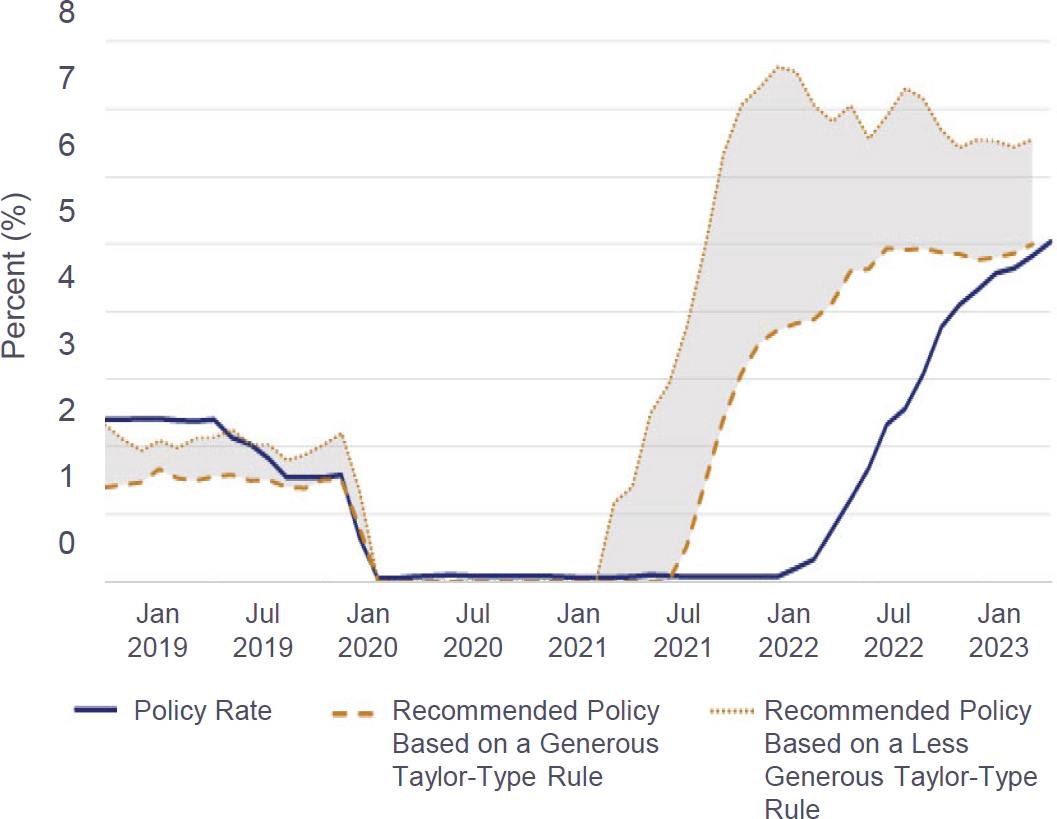

Active policy tightening, which has led to 500bps of rate increases since March 2022, was needed to just catch up to reported inflation. Now that we’ve reached that point, policy has entered restrictive territory (as highlighted by James Bullard, President and CEO of the Federal Reserve Bank of St. Louis in his recent work).

Crossover to “Passive Tightening” as Inflation Cools Below Policy Rate(1)

Actual Policy Rate and Policy Rate Recommendations from Taylor-Type Rules(2)

Recession Calls Get Reset, a Look Back, then Ahead

This new stage of policy tightening coincides with many economic forecasters adjusting their recession calls, from the extreme (taking off their recession calls completely), to the more moderate (lowering recession probabilities, or delaying / shallowing any forthcoming recession). Active debate will ensue on time lags for restrictive policy to take effect.

Recalibrating the recession calls made thus far will factor in the magnitude of stimulative fiscal spending (CHIPS Acts, Inflation Reductions Act etc.), while reduce reliance on the sharp declines in manufacturing indicators - especially as demand shifted from goods to services as the pandemic eased - and on declining money supply indicators, the latter two having worked historically, but not in this cycle.

Looking ahead, the rates market is priced to the Fed easing into 2024, suggesting economic weakness emerging in the second half of 2023, and pushing the Fed to promptly cut rates. This opens the door to two scenarios. Should the market view hold it indicates an imminent recession and quick policy easing that could eventually prevent a hard hit to the economy. The counter, should policy rates keep tightening through the second half, intensifies passive tightening, perhaps delivering a recession as growth slows into stable-to-higher policy rates. This is the risk scenario to recession calls.