Not All Tightening Is Equal: Reading the Cross-Asset Signal

The Rithm Take

Financial conditions have tightened meaningfully as markets respond to the escalation in the Middle East. Equity markets have sold off, high yield spreads have widened, and both bond and equity volatility have increased.

But the tightening has not been uniform. Relative to the repricing seen on Liberation Day last year, the move in traditional asset classes still looks more contained. Oil markets, by contrast, have moved much more aggressively. Oil volatility is substantially higher, and the futures curve suggests the market is pricing a disruption that persists for longer than what is implied by equities and rates.

That’s the current divergence. Traditional markets are acknowledging a tighter backdrop, but oil is pricing a more severe and longer-lasting shock.

Market Signals

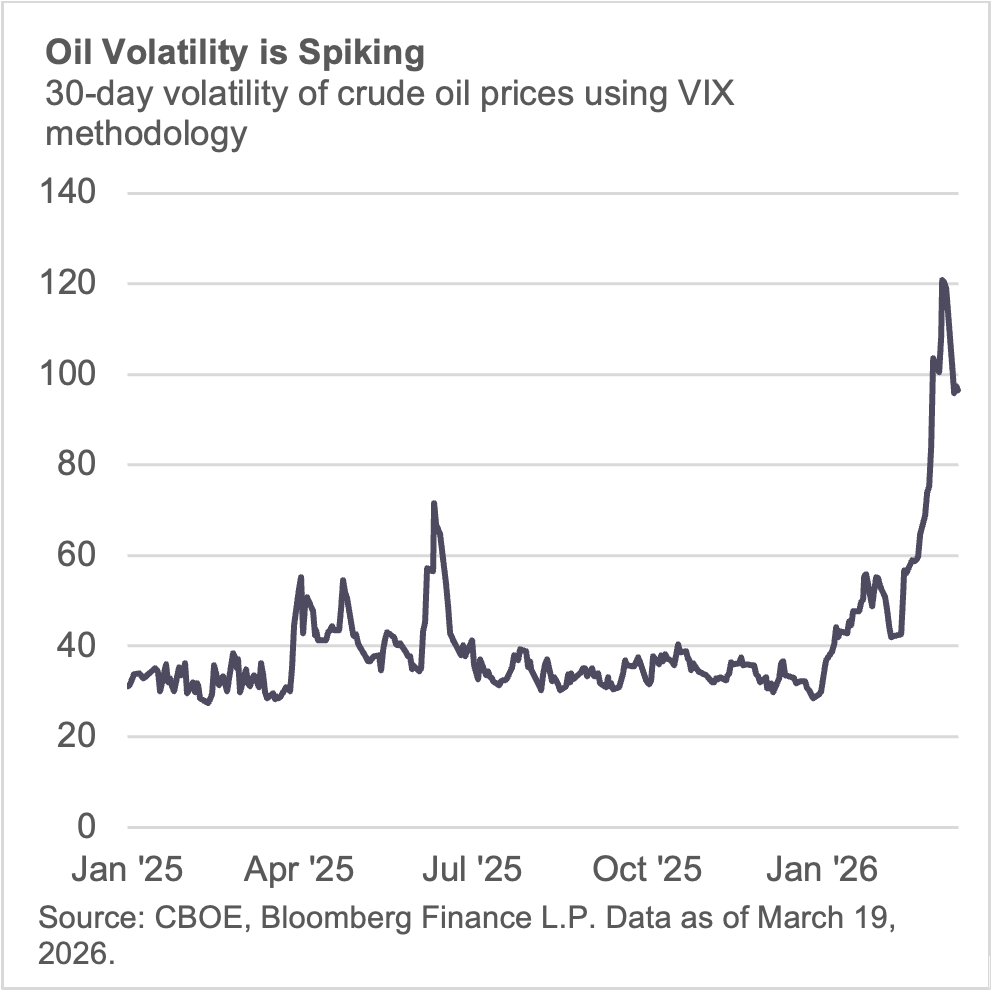

Oil has been the cleanest first-order reaction function to the conflict. That makes sense given the market’s direct sensitivity to Middle East supply risk and, more specifically, the importance of flows through the Strait of Hormuz.

The key point is not just that oil volatility has risen sharply, but that it has risen materially more than volatility in other major asset classes. That suggests energy markets are assigning a meaningfully higher probability to disruption risk than equities or rates.

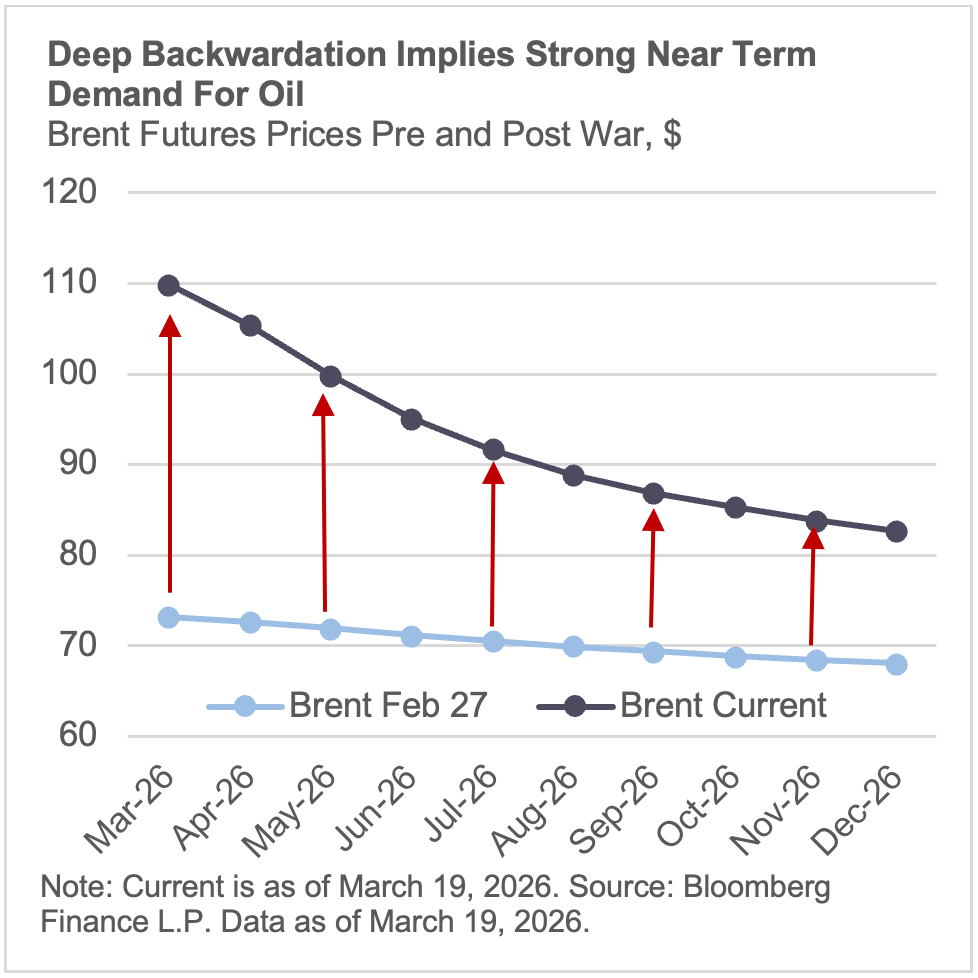

The oil futures curve is in deep backwardation, meaning shorter dated futures prices are above longer term prices, implying a premium for product availability. Commodity “tourist” traders not native to the market may also be driving up near term prices as they look for a hedge. But the more important signal is how long that slope persists.

The curve does not begin to meaningfully flatten until September/October of this year, which suggests the market is pricing near-term tightness that takes time to ease. Said differently, oil is not just pricing disruption, it is pricing disruption with duration.

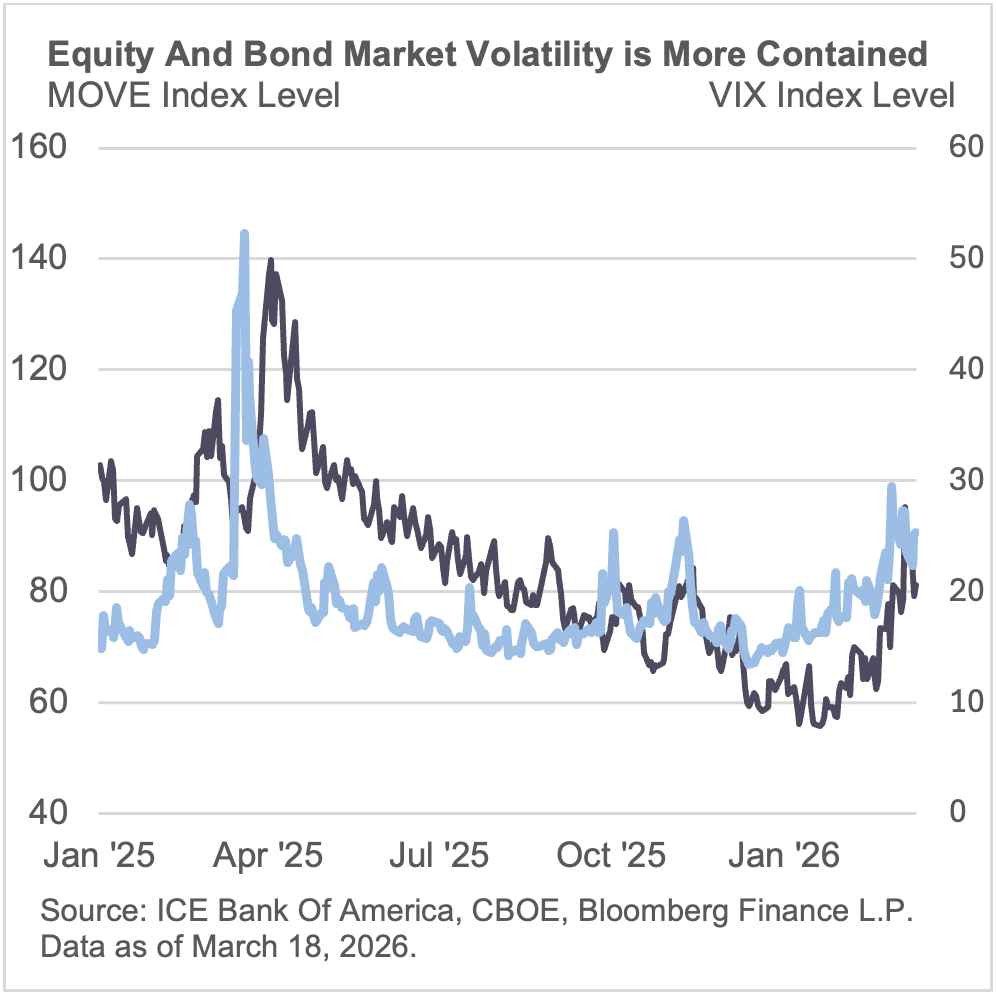

Bond and equity volatility have both moved higher, which confirms that financial conditions are tightening and that the shock is being felt outside of energy.

But the increase remains more moderate than the move seen during Liberation Day. In other words, traditional markets are repricing, but not in a way that suggests they are fully embracing the same level of risk now being reflected in oil.

The S&P 500 remains close to its highs, and the pullback to date looks more like a risk trim than a full reassessment of the macro backdrop.

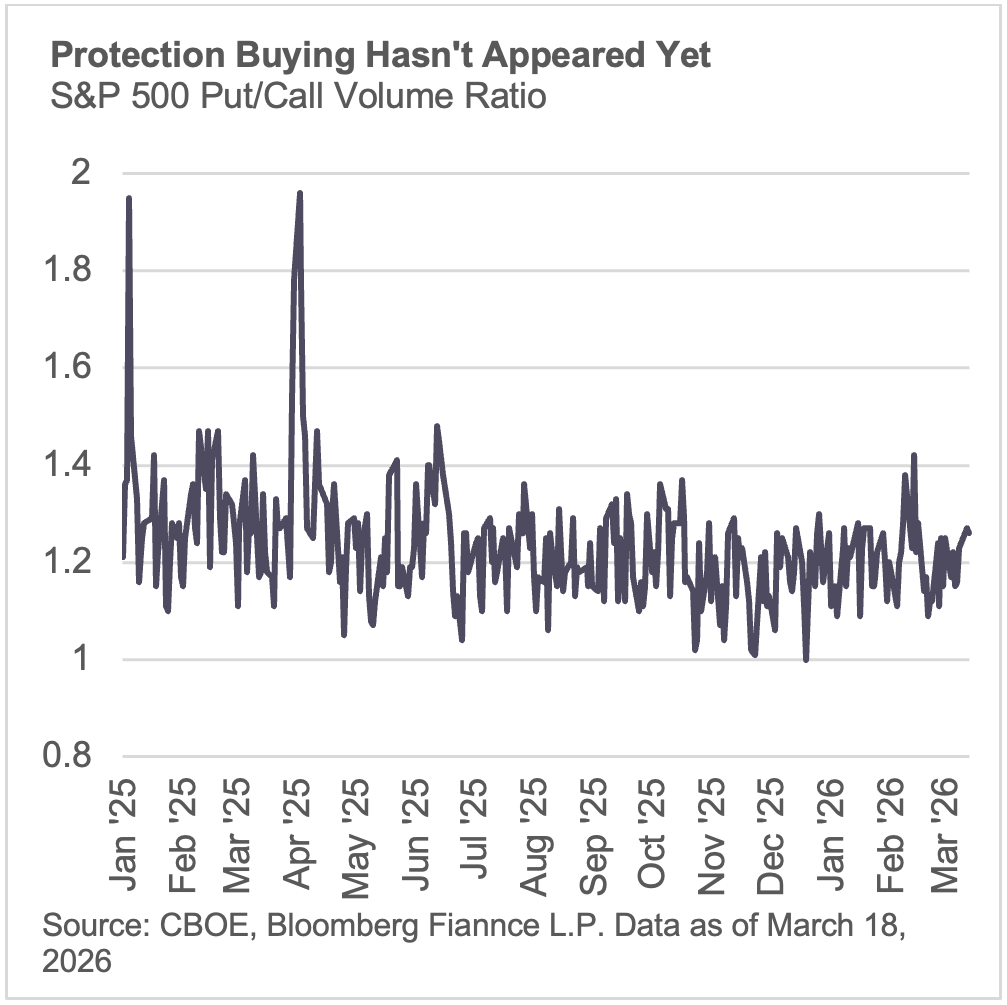

That interpretation is reinforced by options activity. Put/call volume ratios do not suggest an aggressive demand for downside protection relative to prior episodes of market stress.

So while equities have weakened at the margin, they still appear to be pricing a scenario where the conflict is contained and does not meaningfully impair the broader earnings or liquidity backdrop.

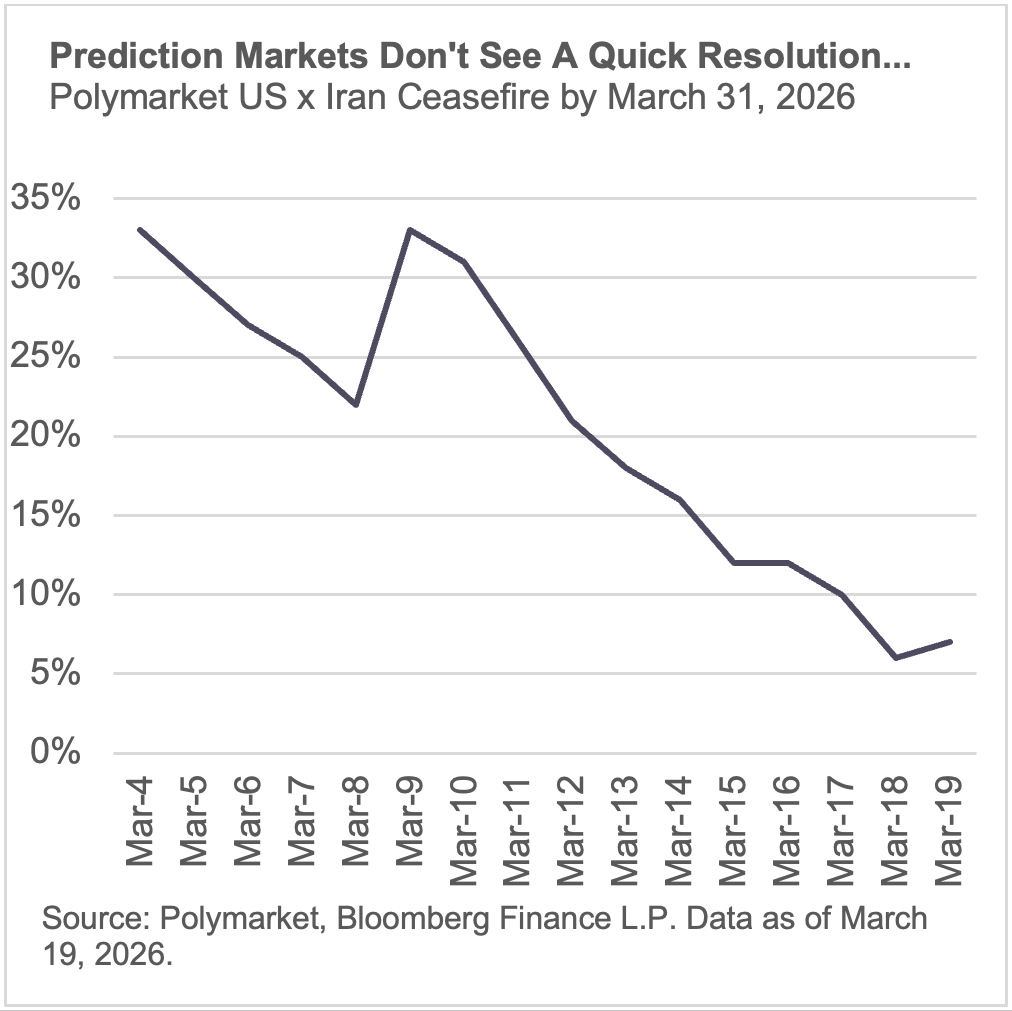

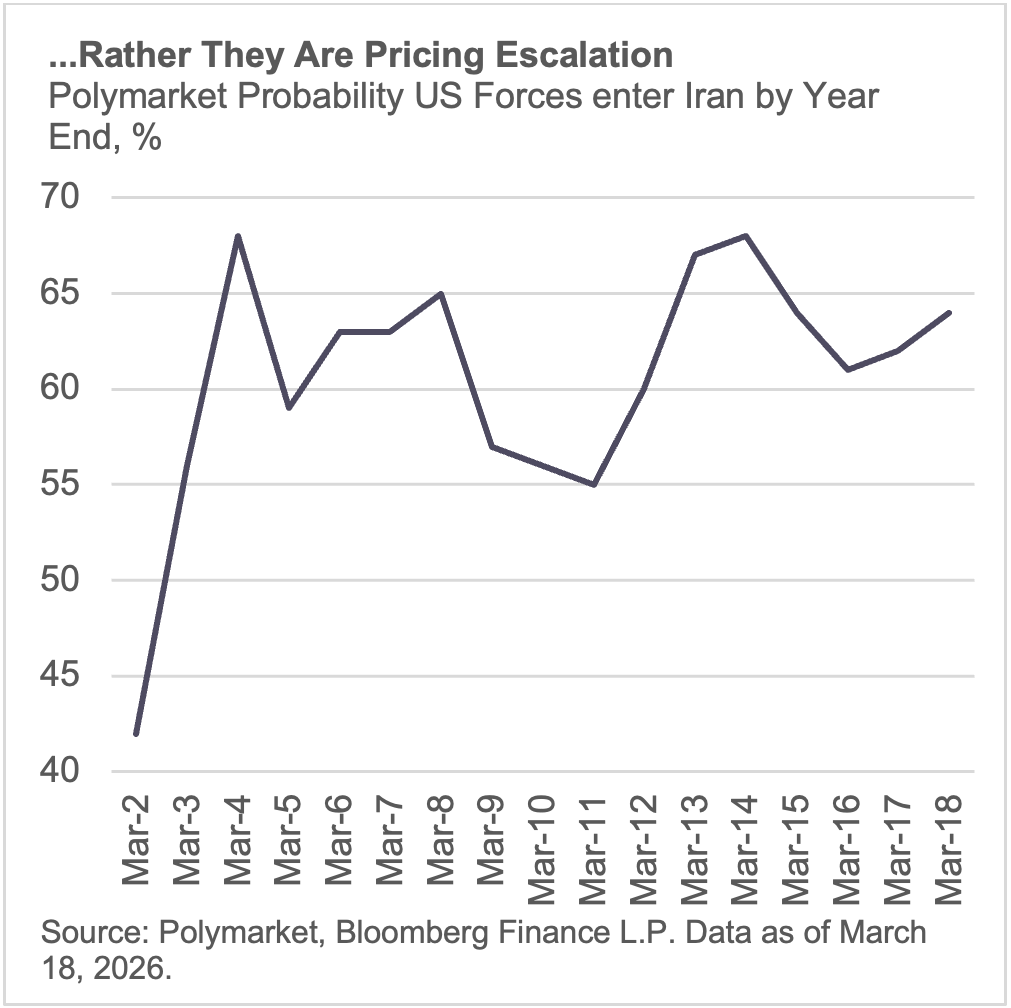

Prediction markets present a more cautious message. The implied probability of a ceasefire by month end remains low, while the probability assigned to a more serious escalation remains elevated.

These markets should not be treated as a base case forecast on their own, but they are useful as a cross-check on timing. Here, they are pointing to a longer and less benign path than what is reflected in most traditional risk assets.

What does it all mean? Tighter financial conditions.

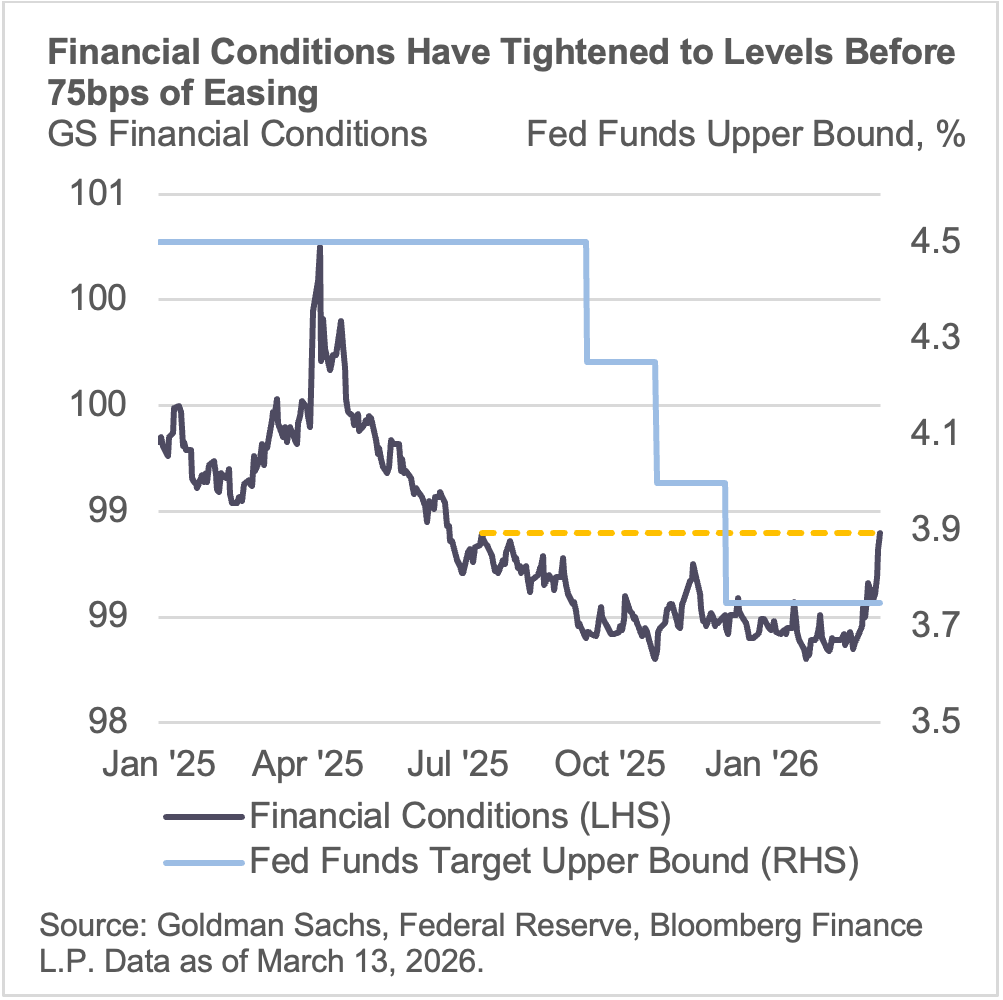

Financial conditions have tightened meaningfully as higher oil prices, wider credit spreads, weaker equities, and higher volatility feed through to the broader market backdrop.

Conditions have now retraced back to levels last seen in July of last year. Since then, the Fed has delivered three rate cuts.

In effect, markets have unwound the equivalent of that easing through a combination of higher volatility, wider spreads, and tighter risk appetite. This underscores that the move is not trivial. Financial conditions have tightened in a way that is macro-relevant.

Bottom line: Markets agree conditions are tighter, but oil is pricing a more severe and longer-duration shock than what is reflected in equities and credit.