Banks and the Rise of ABF: A Partnership, Not a Displacement

The Rithm Take

Recent headlines have put private credit under heightened scrutiny, particularly around liquidity and retail fund structures, but that conversation risks overshadowing the more fundamental shift underway in how credit markets are being built.

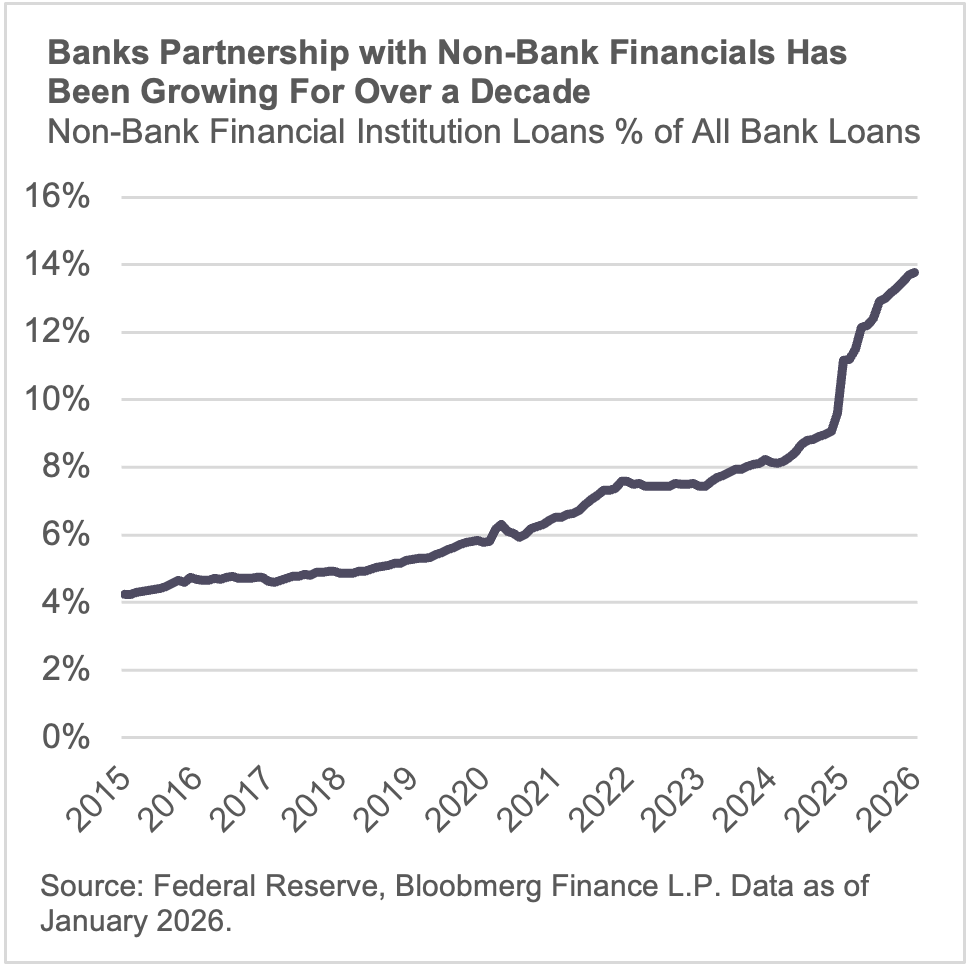

The long-run rise in non-bank financial institutions (NBFI) lending is a signal that this is not a one-cycle trade; it is a durable balance-sheet allocation decision. A steadily rising share over a decade usually means the product has become repeatable, scalable, and operationally embedded. In practice, that tends to happen when exposures are standardized enough to be underwritten through process, monitored through reporting, and renewed through relationships. For ABF, it reads as institutionalization: banks have effectively accepted NBFI/ABF-adjacent facilities as a core banking product rather than episodic or cyclical lending.

The growth has been persistent and structural.

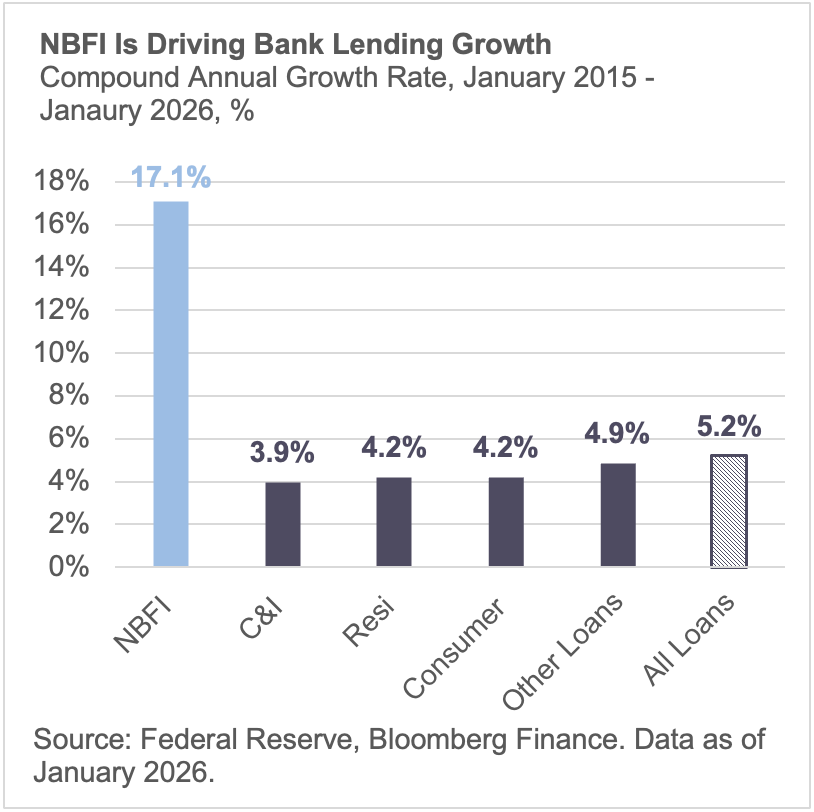

NBFI lending has steadily increased as a percentage of total bank loans while compounding at a multiple of overall loan growth. The trajectory is gradual and sustained rather than cyclical. This is not a late-cycle spike; it is a decade-long reallocation of balance-sheet capacity toward financial intermediaries and collateral-backed structures.

NBFI lending is the marginal growth engine inside bank balance sheets.

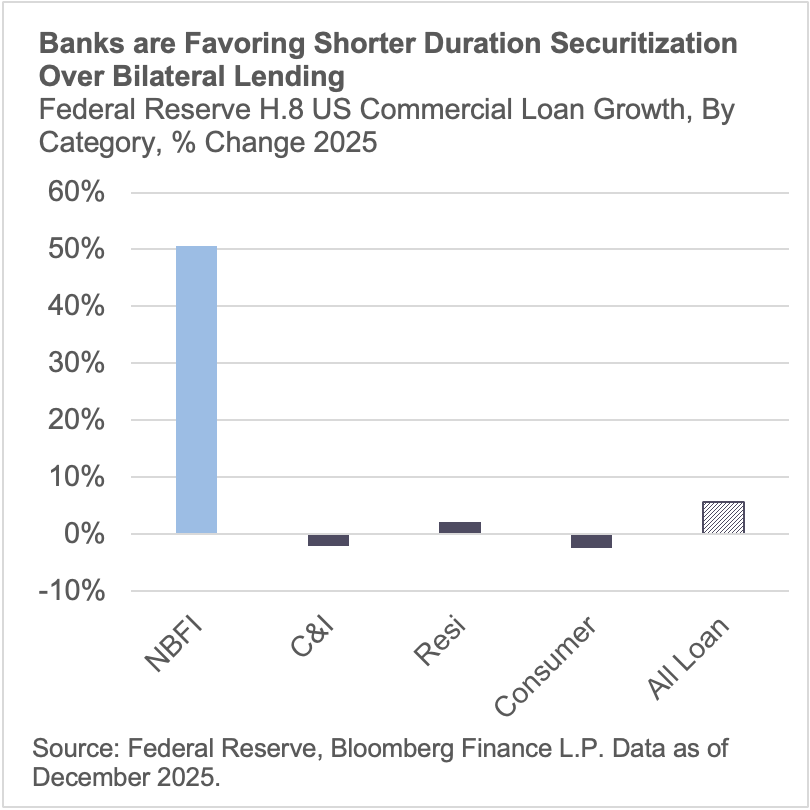

The expansion in total bank lending is being disproportionately driven by NBFI exposures. While other loan categories are stable or modestly growing, the acceleration is concentrated in lending tied to financial platforms. Incremental bank balance-sheet deployment is flowing toward structured finance channels rather than traditional bilateral lending.

Banks are favoring shorter duration and controllable risk profiles.

Many NBFI exposures are structured as warehouse lines, secured revolvers, or collateralized facilities with defined advance rates and eligibility criteria. They are typically floating rate, mark-to-market, and tied to specific asset pools. Compared to traditional operating-company loans, these structures offer clearer collateral controls, shorter effective duration, and identifiable takeout paths through securitization or term financing.

The shift suggests a preference for assets that can be margined, monitored, and potentially distributed, aligning with regulatory and liquidity considerations.

The rise in NBFI lending mirrors the expansion of asset-based finance.

ABF requires warehouse capacity to originate and aggregate assets before terming them out. As ABF scales, secured bank facilities scale alongside it. The growth in NBFI lending therefore reads as throughput in the ABF system – the expansion of one mechanically drives growth in the other.

This reflects a partnership model rather than displacement.

Banks are increasingly funding platforms and collateral pools, while alternative managers control underwriting and servicing. Credit is moving through banks, not off them. The acceleration in NBFI lending is the balance-sheet expression of that modular system becoming institutionalized.

The takeaway is straightforward: NBFI lending is no longer a side channel — it is the balance-sheet expression of how modern credit markets are structured. As banks fund platforms and collateral pools, asset-based finance is becoming embedded in the core of the banking system.