An Easy Decision in a Complicated World

The Rithm Take

We expect the Fed will hold next week, and it should. The more interesting question is how the Committee characterizes the balance of risks in a world where core inflation is running above target, an oil shock has arrived, and the employment picture is shaky. That framing, more than any individual data point, will set the tone for how markets think about the remainder of the year.

Market Signals

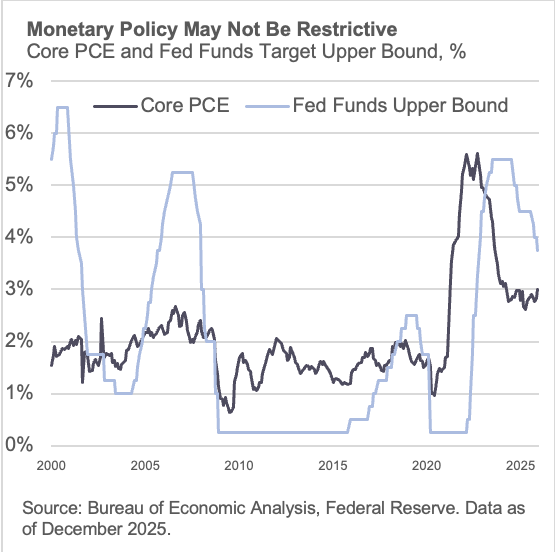

When the conflict started on February 28, futures markets had nearly 2.5 rate cuts priced for 2026. That's now been cut to less than one. The 10-year Treasury yield has moved higher by ~30-basis-point rise split relatively evenly between higher real yields and wider inflation breakevens. With core PCE at 3.0% and the fed funds midpoint at 3.625%, monetary policy is probably not restrictive and may actually be accommodative.

The Conversation

I. The Economy and unemployment stable

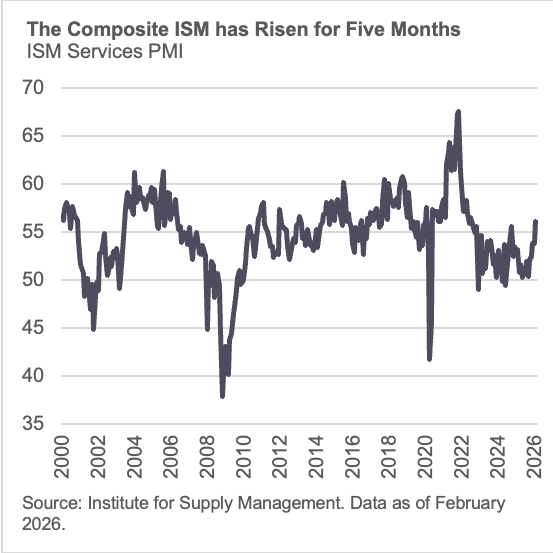

The five-month recession risk has been fairly benign. Since September, the unemployment rate has moved sideways, down to 4.3% in January and back to 4.4% in February. The FOMC's January statement quietly upgraded its characterization from "edged up" to "stabilized," and the data since have validated that language. Private payroll growth has averaged only 28,000 per month over that stretch, a pace that historically would have signaled rising unemployment or early recession. But there are no other recession signals. The composite ISM has risen in each of the past five months to the fastest pace since July 2022. Output is expanding. Profits are solid. The slow job creation reflects very low hiring rather than elevated layoffs; claims data and JOLTS confirm it. Unusual, but not distress.

Then came February 28.

II. Inflation a risk

Crude oil is roughly $25 per barrel higher since the conflict with Iran began. If sustained, that's approximately an 80-cent-per-gallon increase in gasoline prices and a further lift to headline inflation, arriving on top of tariffs that have already kept core PCE at 3.0% for two years. The Strait of Hormuz is two miles wide, but roughly a fifth of global oil supply transits through it. How long this lasts is genuinely unknowable, and that uncertainty cuts both ways. The current market view held is a resolution could see oil retrace quickly, removing much of the inflation impulse before it shows up meaningfully in the data.

III. The Fed likely to look through inflation

The Fed has reasonable grounds to look through a cost shock of uncertain duration. American energy self-sufficiency limit the growth damage that higher oil would have caused in prior decades, and if the conflict de-escalates, the price signal may prove short-lived. At the same time, the historical record offers some caution. Treating oil shocks as transitory has complicated the Fed's job before, and core PCE has now been above target for four years running. The honest answer is that the inflation risk is real but the path is genuinely uncertain, and the Fed is not obviously wrong to hold its framework steady while it waits for more clarity.

IV. Bar for cuts is higher

What does seem clear is that the bar for cuts in the near term has moved higher. Markets have already repriced accordingly. The debate for the rest of the year is less about whether the Fed eases and more about whether the current level of policy is actually doing much work given where growth and asset prices sit.

V. Regulatory policy matters

Running alongside the rate debate is a potential structural tailwind for credit markets that bears watching. The current regulatory posture appears increasingly favorable toward rolling back the Basel III endgame capital requirements, which had proposed forcing the largest U.S. banks to hold significantly more capital against risk-weighted assets. If those requirements are scaled back as currently seems possible, banks that have been defensively managing balance sheet capacity in anticipation of higher requirements could have meaningfully more room to deploy. The potential effects are broad: expanded lending capacity, improved economics for holding assets including mortgages and structured products, and a reduced incentive to distribute risk purely for regulatory relief. For mortgage and asset-backed markets, a more capital-efficient banking system could mean a wider and more competitive set of buyers, which would be a structural positive for spreads and availability. Nothing is final, and the scope of any changes could come imminently. But if the regulatory trajectory continues in its current direction, it represents one of the more meaningful pro-growth developments for credit markets in the outlook, operating largely independent of where the Fed ultimately lands on rates.

Chair Powell's press conference will be the real event. How he characterizes the balance of risks given the oil shock, and how much flexibility he signals for the back half of the year, will tell markets more than the decision itself.