A Tale of Three Markets

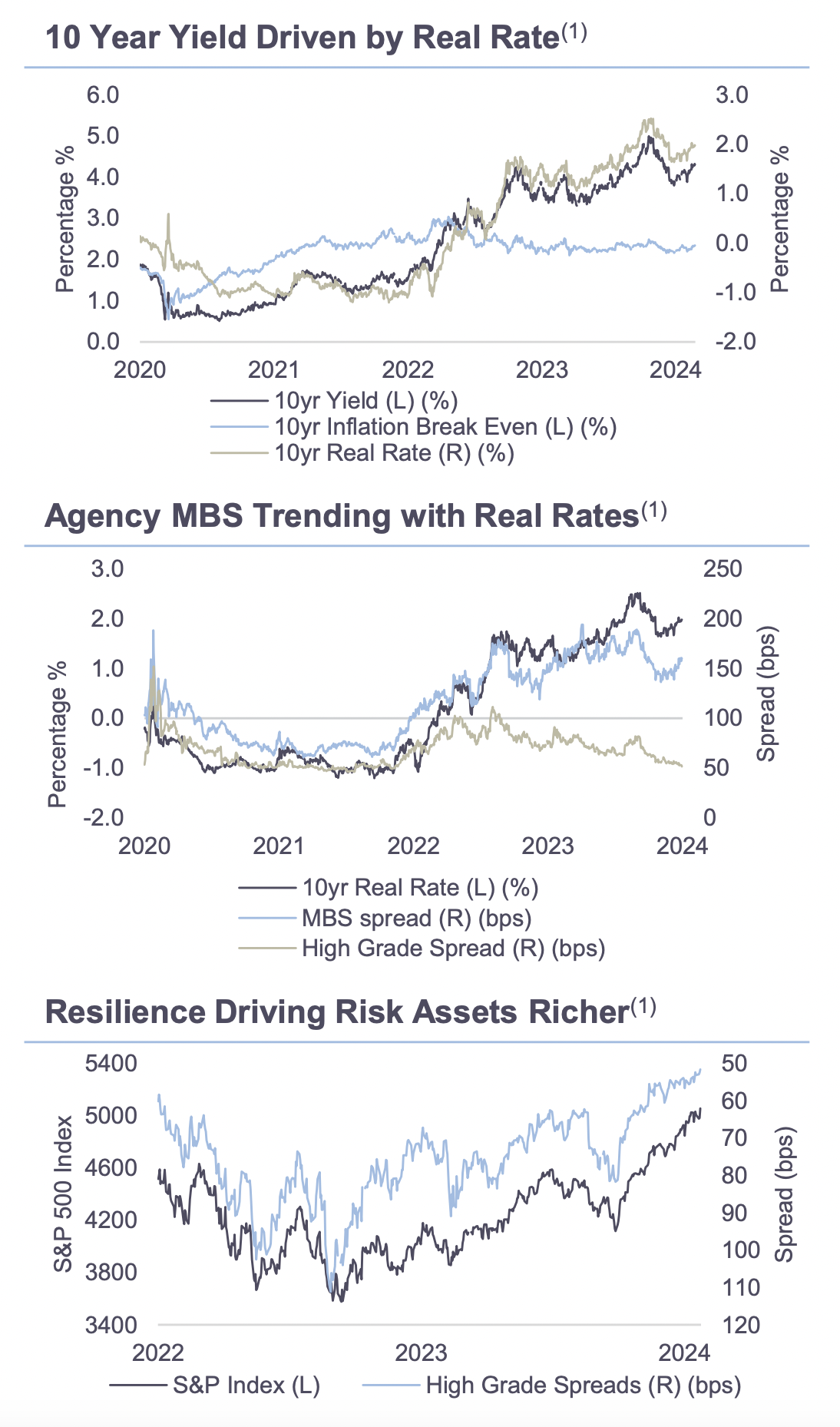

While the recession versus resilience debate remains unresolved, risk-free and risk markets are squarely priced to resilience, as economic data so far this year has supported. The 10-year yield, at 4.33%, sits just above the midpoint of 2023’s low and high points. Agency MBS spreads are wide while high-grade spreads and stocks are at respective tights and record highs, all priced to resilience.

The Conversation

The nominal 10-year yield swung from a low of 3.3% to a high of 5% between April to October 2023 as the market recovered post-SVB to strong economic data. Entirely driving nominal yields over the last two years is the real rate. Inflation expectations, on the other hand, have remained stable. At just under 2%, this real rate is 50bps below the 2.5% peak in late 2023, but far higher than the -1.1% level that prevailed at the end of 2021. Implied forward nominal yields are at or below current 10-year yields for the next two years and implied inflation breakevens are stable around 2%, indicating stable real rates ahead, a nod to a soft landing outcome and Fed credibility.

Not benefiting from this resilience is agency MBS spreads, which remain persistently wide and trending with higher real rates. Uncertainty on monetary policy drives volatility higher. Additionally, the Federal Reserve’s balance sheet runoff (Quantitative Tightening) is adding to the supply money managers, the price sensitive buyers, have to purchase. Risk of more supply from bank portfolio restructurings, like Truist announced last week, further cloud the technical picture. Certainty on these factors or a clear sign of economic weakness is needed to see these optically cheap valuations normalize.

On the flip side, setting new records and multi-decade tights respectively are stock and high-grade credit. Economic resilience and strong earnings have supported richening valuations in these sectors.

The Rithm Take

The Atlanta Fed's GDPNow estimate for the first quarter, at 2.9%, suggests that growth has slowed from the average pace of 4.1% in the second half of 2023, it is still running ahead of the 2.2% pace seen in the first quarter of last year. Additionally, The ISM New Orders to Inventories is on an upswing, which risk assets trend to, and stands to lend support to the resilience view holding on for longer, driving valuations richer.