A Lighter Constraint, Not a Structural Shift: Interpreting Mortgage Capital Reform

The Rithm Take

The Fed’s proposed overhaul of bank capital rules moves in a clear direction. Capital treatment is becoming more risk-sensitive and, at the margin, less punitive for certain lending activities, including mortgages. The implication for the mortgage market, however, is more incremental than transformative.

While the proposal lowers capital intensity in key areas, particularly for high-quality loans and servicing, the changes are best understood as removing friction rather than fundamentally reshaping bank behavior. Banks are being given more flexibility to engage, but not a strong enough economic incentive on its own to drive a broad-based re-entry into mortgages.

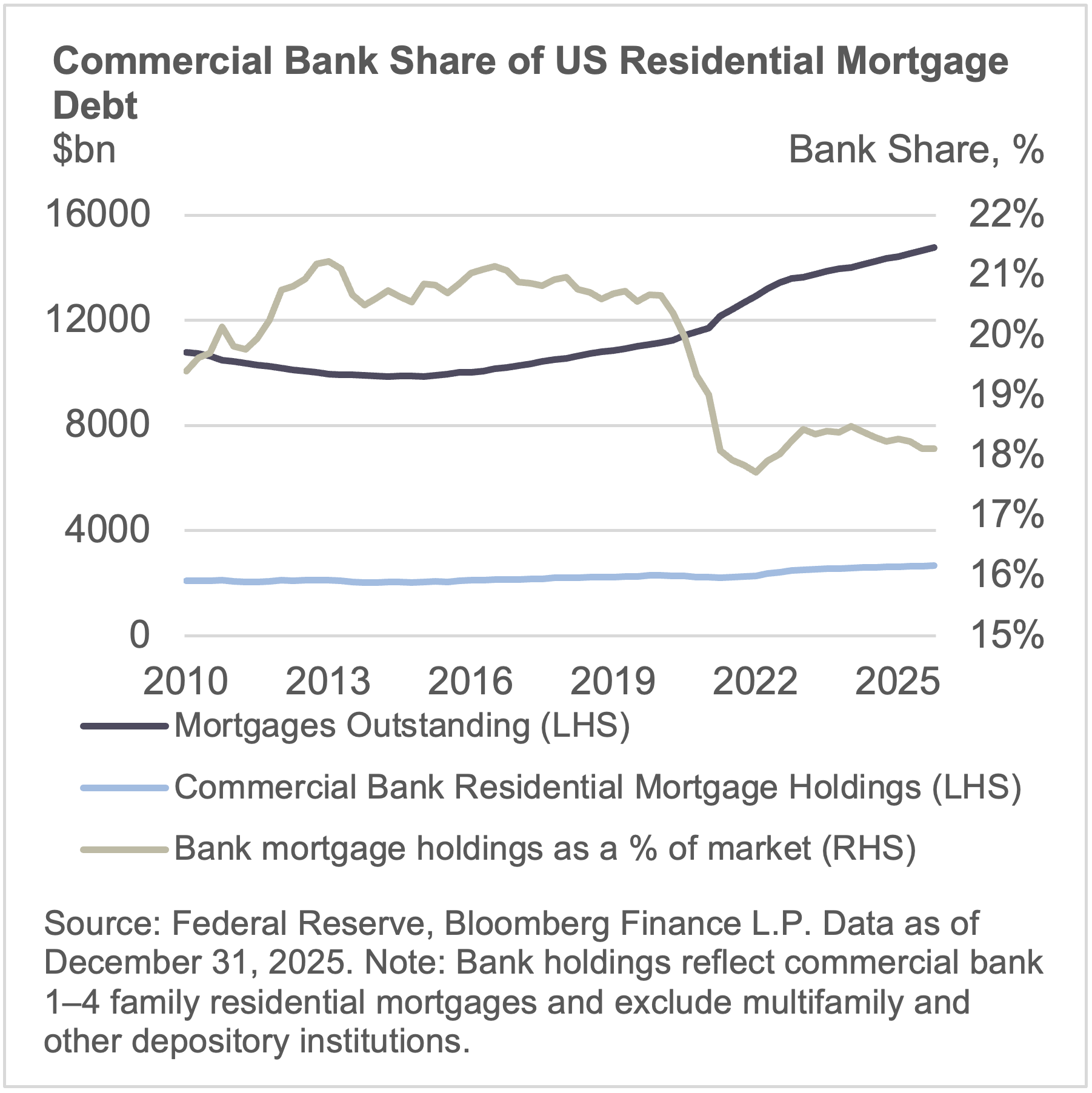

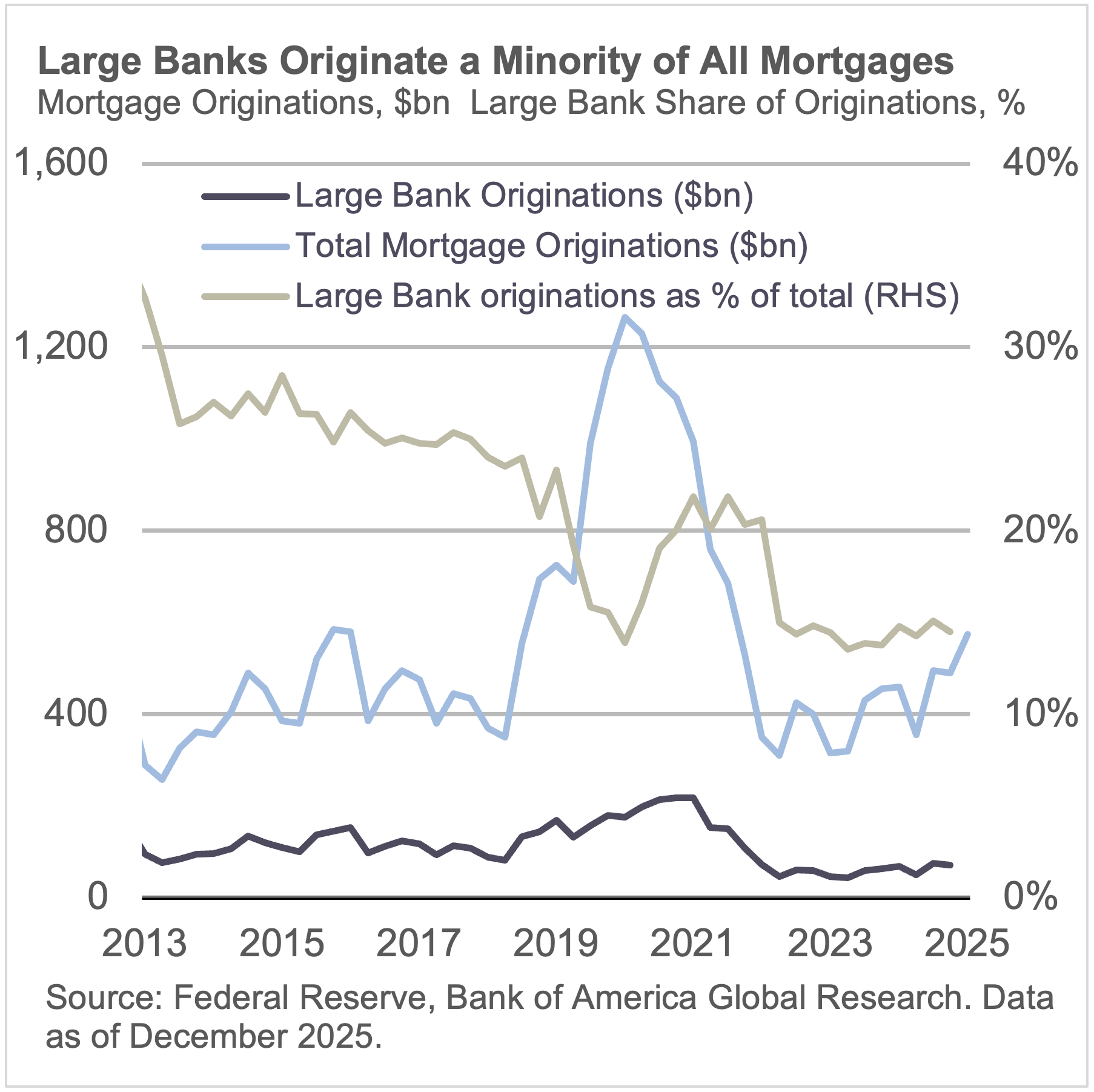

The more relevant question is where these changes actually matter. On balance, the proposal is supportive for mortgage lending and servicing, but the impact is selective and segment-specific, with the clearest effects in prime conventional lending and certain servicing strategies. The broader structure of the mortgage market, where nonbanks play a central role, remains intact.

Proposed Cumulative Change to Aggregate CET1 Capital Requirements

|

Category |

Category I and II firms |

Category III and IV firms |

Smaller banking organizations |

|---|---|---|---|

|

Basel III NPR |

1.40% |

|

|

|

GSIB Surcharge NPR |

-3.80% |

|

|

|

Revised Standardized Approach |

|

-6.10% |

-7.80% |

|

AOCI Requirement |

|

3.10% |

|

|

Proposed Stress Test Changes |

-4.3% (global market shock & operational risk); +1.9% (other changes) |

-2.20% |

|

|

Total |

-4.80% |

-5.20% |

-7.80% |

Source: Federal Reserve

Market Signals

1.The proposal reduces capital requirements across bank categories by mid-single digits. This creates incremental balance sheet capacity, but not to a degree that forces a reallocation into mortgages. It improves optionality rather than dictating behavior.

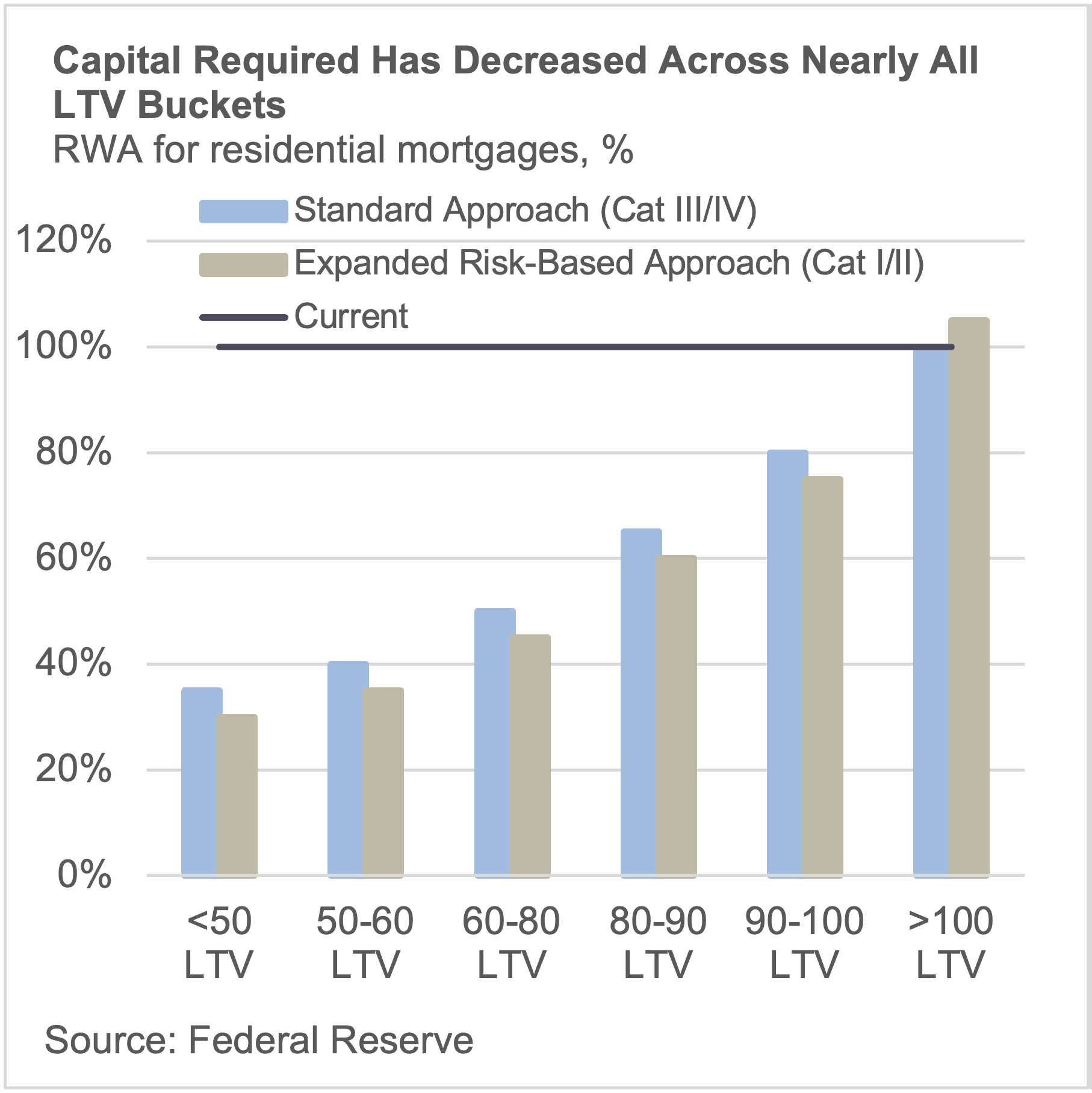

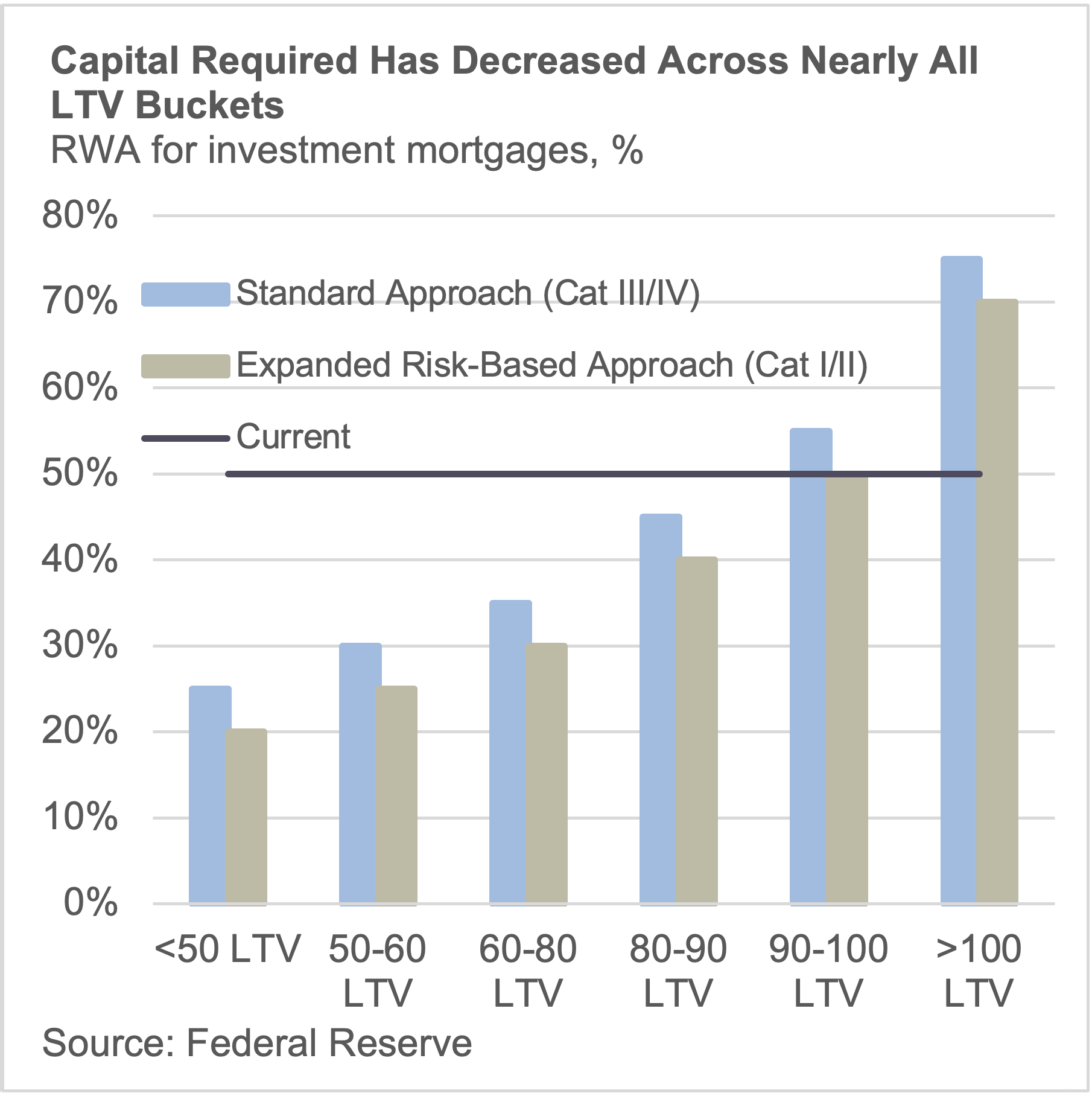

2. Risk-sensitive mortgage treatment improves economics at the margin. The shift to LTV-based risk weights lowers capital charges for lower-LTV loans, particularly in prime conventional segments. This better aligns capital with credit risk, but primarily benefits already attractive loan cohorts rather than opening up new areas of lending.

3. Lifecycle economics improve, but gradually. Recognizing amortization allows capital requirements to decline as loans season. This supports hold economics over time, but the benefit accrues slowly and does not materially change near-term origination decisions.

4. Servicing becomes more manageable, not materially cheaper. The removal of the CET1 deduction threshold for MSAs eliminates a structural constraint, but the 250% risk weight remains. Servicing becomes easier to scale within banks, but it is not suddenly capital-light. The change supports incremental participation rather than a step-change in ownership.

5. Competitive effects are concentrated in prime segments. The proposal most directly impacts conventional and jumbo lending, where capital treatment improves and banks already have infrastructure advantages. Government lending and more operationally intensive segments remain largely unchanged, preserving nonbank advantages. The result is localized competitive pressure, not a market-wide shift.

Bottom Line: The Fed’s proposal adjusts the rules of engagement rather than resetting them.

- Mortgage lending and servicing become modestly more attractive for banks, particularly in high-quality, low-LTV segments. That should support incremental increases in bank activity over time, especially in conventional and jumbo markets.

- The changes are not large enough on their own to drive a broad re-entry or displace existing market structure. Nonbanks remain central to the ecosystem, particularly in government lending and servicing-intensive segments.

- Securitization impact is mixed. Lower capital on mortgages incentivizes banks to hold more loans, reducing supply, but increased lending capacity could offset this if origination volumes rise. The net effect depends on whether banks shift toward hold or continue to distribute.

- The practical implication is narrower. Competition tightens at the margin in select areas rather than across the entire mortgage market. The evolution is gradual, and execution, not regulation, will determine how much of this incremental capacity ultimately translates into lending.